Subprime auto lenders for 500 credit score? Yeah, it’s a rough spot, but not a dead end. This isn’t your typical car loan situation; we’re talking about lenders who specialize in helping people with less-than-perfect credit get behind the wheel. We’ll break down what that means, the risks involved, and how to navigate this tricky terrain to get the best deal possible.

Think of it as a survival guide for the financially challenged car buyer.

We’ll explore the world of subprime auto loans, dissecting the terms, interest rates, and potential pitfalls. We’ll also cover alternative financing options and strategies to improve your credit score so you can escape the subprime cycle. Whether you’re already facing this situation or just want to understand the landscape, this guide’s got you covered.

Understanding Subprime Auto Lending

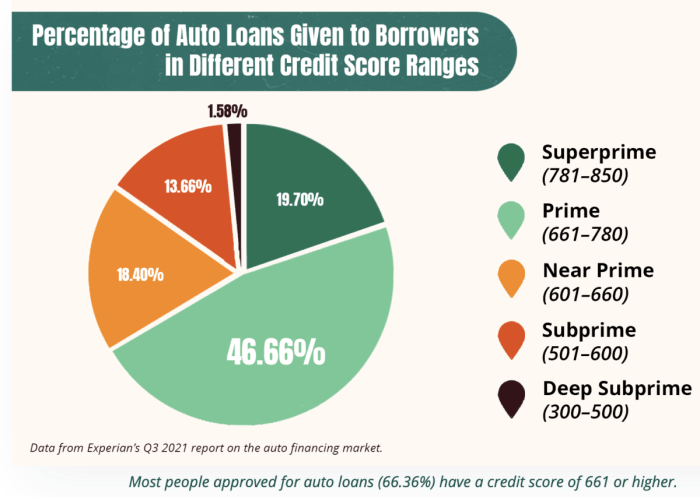

Subprime auto lending is a segment of the auto finance industry that caters to borrowers with poor credit histories, typically those with credit scores below 660. These loans are characterized by higher interest rates and stricter terms compared to loans offered to borrowers with better credit. Understanding the nuances of this market is crucial for both lenders and borrowers, as it involves significant financial risks and potential consequences.

Characteristics of Subprime Auto Loans

Subprime auto loans are designed for individuals who have difficulty securing financing through traditional channels. Key characteristics include significantly higher interest rates reflecting the increased risk of default, shorter loan terms (often 36-48 months), and potentially higher fees, including origination fees, late payment fees, and prepayment penalties. Lenders often require larger down payments to mitigate risk. These loans are frequently secured by the vehicle itself, meaning the lender can repossess the car if payments are missed.

The availability of subprime auto loans provides access to credit for individuals who might otherwise be excluded from the auto market, but it comes at a significant cost.

Risks Associated with Lending to Borrowers with 500 Credit Scores

Lending to borrowers with 500 credit scores presents substantial risk for lenders. A 500 credit score indicates a history of significant financial difficulties, including missed payments and potential bankruptcies. This dramatically increases the probability of loan default, meaning the borrower will fail to make payments. Repossession is a common outcome, but the process is costly and time-consuming for lenders.

The value of the vehicle may depreciate quickly, resulting in a net loss for the lender even after repossession. Furthermore, the administrative costs associated with managing delinquent accounts add to the overall risk. The lender must carefully assess the borrower’s ability to repay the loan, even with the higher interest rates and fees.

Typical Terms and Conditions of Subprime Auto Loan Agreements

Subprime auto loan agreements often include terms such as high annual percentage rates (APRs), typically ranging from 15% to 25% or even higher, depending on the borrower’s credit score and the lender’s risk assessment. Loan terms are usually shorter than prime loans, often ranging from 36 to 60 months. Balloon payments, a lump sum payment due at the end of the loan term, are sometimes included.

Prepayment penalties may be imposed if the borrower pays off the loan early. Gap insurance, which covers the difference between the vehicle’s value and the loan amount in case of a total loss, is frequently offered but at an added cost. Late payment fees are typically substantial. The lender may also require full-coverage insurance on the vehicle.

Comparison of Subprime and Prime Auto Loans

Prime auto loans are offered to borrowers with good credit scores (typically 660 or higher). They feature significantly lower interest rates (often below 5%), longer loan terms (up to 72 or 84 months), and fewer fees. Borrowers with prime credit typically qualify for better terms and conditions. The approval process is also generally faster and less stringent for prime loans.

In contrast, subprime auto loans are designed for higher-risk borrowers and come with substantially higher costs and stricter requirements. The key difference lies in the risk assessment and the resulting pricing of the loan.

Example Subprime Auto Loan Rates and Terms

| Lender | APR | Loan Term (Months) | Typical Fees |

|---|---|---|---|

| Example Lender A | 18-22% | 36-48 | $500-$1000 origination fee, late payment fees |

| Example Lender B | 20-25% | 48-60 | $750-$1500 origination fee, prepayment penalty |

| Example Lender C | 15-20% | 36 | $300-$700 origination fee, late payment fees |

Note: These are example rates and fees and may vary significantly based on individual creditworthiness, lender policies, and market conditions. It’s crucial to shop around and compare offers from multiple lenders before committing to a loan.

Borrower Profile and Financial Implications

A 500 credit score signifies significant financial challenges and places borrowers in a high-risk category for lenders. Securing an auto loan at this score often means accepting significantly higher interest rates and potentially unfavorable loan terms within the subprime auto lending market. Understanding the typical borrower profile and the financial implications involved is crucial for both lenders and potential borrowers.Individuals with a 500 credit score often grapple with a history of missed payments, high debt-to-income ratios, and limited savings.

Their financial situation is typically precarious, making them vulnerable to further financial hardship if they default on their auto loan. The consequences of default can be severe, including repossession of the vehicle, damage to their credit score (making future borrowing even harder), and potential legal action.

Typical Financial Situation of a 500 Credit Score Borrower

Borrowers with a 500 credit score often find themselves in a cycle of debt. They may have multiple outstanding loans, high credit card balances, and possibly past bankruptcies or foreclosures. Their income may be inconsistent or barely cover their essential living expenses, leaving little room for unexpected costs or debt repayment. Many struggle with budgeting and financial planning, leading to further financial instability.

For example, a borrower might be working a minimum wage job, juggling rent, utilities, and child care costs, leaving minimal funds available for debt repayment. This precarious financial position makes them heavily reliant on subprime lenders for financing, despite the high cost.

Consequences of Defaulting on a Subprime Auto Loan

Defaulting on a subprime auto loan has far-reaching negative consequences. The most immediate is the repossession of the vehicle, leaving the borrower without transportation and potentially impacting their ability to work. Furthermore, the default will severely damage their credit score, making it even more difficult to obtain credit in the future for necessities like housing or other loans.

Late payments and collections will be reported to credit bureaus, further hindering their ability to improve their financial situation. In some cases, the lender may pursue legal action to recover the outstanding debt, potentially leading to wage garnishment or a judgment against the borrower. The financial ramifications can be long-lasting and difficult to overcome.

Finding subprime auto lenders with a 500 credit score is tough, but it’s doable. Getting approved often means higher interest rates, so lowering your overall expenses is key. That’s why managing car insurance is crucial; check out this guide on How to lower car insurance after a DUI 2025 for some tips, even if you haven’t had a DUI.

Lowering your insurance can free up cash to tackle those higher auto loan payments, making the whole process a bit less stressful.

Factors Contributing to a 500 Credit Score

A 500 credit score usually results from a combination of negative financial behaviors over time. Common factors include a history of missed or late payments on loans and credit cards, high credit utilization (using a large percentage of available credit), multiple bankruptcies or foreclosures, and a lack of established credit history. These factors indicate a pattern of irresponsible financial management and significantly reduce a borrower’s creditworthiness.

For instance, consistently paying bills late, even by a few days, negatively impacts credit scores. Similarly, maxing out credit cards demonstrates poor financial discipline and increases risk for lenders.

Strategies for Improving Credit Scores

Improving a 500 credit score requires a proactive and disciplined approach to financial management. This involves paying down existing debt, paying all bills on time, consistently monitoring credit reports for errors, and utilizing credit responsibly. Creating a realistic budget and sticking to it is crucial. Exploring credit counseling services can provide guidance on debt management and financial planning.

Gradually building a positive credit history through responsible credit use will gradually improve the credit score over time. Using secured credit cards or becoming an authorized user on a credit card with a good payment history can also contribute to improving credit scores.

Hypothetical Budget for a Borrower with a 500 Credit Score

Let’s assume a borrower earns $2,500 per month. A responsible budget would prioritize essential expenses:

| Expense Category | Amount |

|---|---|

| Rent/Mortgage | $800 |

| Utilities | $200 |

| Groceries | $400 |

| Transportation (excluding loan payment) | $150 |

| Debt Repayment (minimum payments) | $300 |

| Savings | $100 |

| Miscellaneous | $550 |

This budget allocates funds to essential needs while leaving a small amount for savings and unexpected expenses. It’s crucial to prioritize debt repayment to reduce the overall debt burden and improve creditworthiness. This example demonstrates responsible debt management, a critical step in improving credit scores. The “Miscellaneous” category allows for flexibility while encouraging mindful spending. Note that this is a simplified example and should be adjusted based on individual circumstances.

Lender Practices and Regulations: Subprime Auto Lenders For 500 Credit Score

The subprime auto lending market operates within a complex regulatory framework designed to protect consumers while allowing lenders to manage risk. However, the balance between these two goals is often debated, and the effectiveness of regulations varies. This section explores the regulatory environment, responsible lending practices, risk assessment methods, and potential red flags for borrowers.

Regulatory Environment of Subprime Auto Lending

Subprime auto lending is subject to various federal and state laws, primarily focused on fair lending practices and consumer protection. The Consumer Financial Protection Bureau (CFPB) plays a significant role, enforcing laws like the Truth in Lending Act (TILA) and the Equal Credit Opportunity Act (ECOA). These laws mandate clear disclosure of loan terms, prohibit discrimination in lending, and establish requirements for responsible lending practices.

State-level regulations often add further layers of protection, varying in their specifics across different jurisdictions. Enforcement of these regulations can be challenging, and lenders’ adherence to them varies. For example, the CFPB has taken action against several lenders for engaging in predatory lending practices targeting subprime borrowers.

Responsible Lending Practices for Subprime Borrowers

Responsible lending practices for subprime borrowers emphasize transparency and fairness. Lenders should clearly disclose all loan terms, including interest rates, fees, and payment schedules, in a way that is easily understandable. They should also assess the borrower’s ability to repay the loan before approving it, considering factors beyond credit score, such as income, expenses, and debt-to-income ratio. Responsible lenders avoid practices like steering borrowers towards loans with excessively high interest rates or fees solely because of their credit score.

Offering financial literacy resources and counseling to borrowers can also be considered a responsible lending practice, equipping them with the tools to manage their debt effectively.

Risk Assessment Methods for Subprime Borrowers

Lenders use various methods to assess the risk of subprime borrowers, going beyond a simple credit score check. These methods often involve a more thorough review of the borrower’s financial situation, including income verification, employment history, and debt analysis. Alternative credit scoring models, which incorporate factors like rental payment history or utility bill payments, are also increasingly used to provide a more comprehensive view of a borrower’s creditworthiness.

Some lenders utilize sophisticated algorithms and predictive modeling to assess the probability of default, combining various data points to create a risk profile for each borrower. The use of these models, however, can lead to biases if not carefully designed and monitored.

Comparison of Lending Practices Across Subprime Auto Lenders

Subprime auto lenders vary significantly in their lending practices. Some prioritize speed and volume, potentially overlooking crucial risk assessment steps. Others focus on building long-term relationships with borrowers, offering financial education and support. Interest rates and fees can differ substantially among lenders, reflecting their varying risk tolerance and business models. Some lenders may specialize in certain types of borrowers or vehicles, while others have a broader approach.

Comparing offers from multiple lenders is crucial for subprime borrowers to secure the most favorable terms. This requires diligent research and careful comparison of loan agreements.

Red Flags in Subprime Auto Lending

Borrowers should be aware of several red flags that may indicate predatory lending practices. These include extremely high interest rates significantly above market averages, hidden fees or charges not clearly disclosed upfront, aggressive sales tactics pressuring borrowers to sign contracts quickly, and a lack of transparency regarding loan terms and conditions. If a lender is unwilling to answer questions clearly or provides vague or contradictory information, it’s a significant red flag.

Difficulty in contacting the lender or obtaining clear explanations of loan details should also raise concerns. Borrowers should always carefully review loan documents before signing, seeking independent advice if necessary.

Finding a subprime auto lender with a 500 credit score is tough, but not impossible. Before you even start shopping around, though, you should totally use a car loan calculator with taxes and fees to get a realistic idea of your monthly payments. This will help you avoid getting slammed with unexpected costs and navigate the subprime lender landscape more effectively.

Knowing what you can realistically afford is key when dealing with higher interest rates.

Alternatives to Subprime Auto Loans

Securing an auto loan with a 500 credit score can feel like navigating a minefield, but subprime loans aren’t your only option. Several alternatives exist, each with its own set of pros and cons. Choosing the right path depends on your financial situation and willingness to invest time and effort in improving your credit.Exploring these alternatives can lead to better interest rates and overall loan terms compared to a high-interest subprime loan.

It’s crucial to weigh the advantages and disadvantages carefully before making a decision.

Secured Loans

Secured loans require collateral, meaning you pledge an asset (like a savings account or other vehicle) to guarantee the loan. This reduces the lender’s risk, making approval more likely even with a low credit score. However, if you default, you risk losing the collateral. For example, using a savings account as collateral could mean losing a significant portion of your savings.

The interest rates are typically lower than subprime loans but higher than those offered to borrowers with excellent credit.

Credit Unions

Credit unions often offer more flexible lending options than traditional banks, sometimes working with borrowers who have lower credit scores. They frequently prioritize member relationships and may be more willing to consider factors beyond just your credit score. However, membership requirements might exist, and loan amounts and terms may still be limited depending on your credit history.

Co-Signer Assistance

Having a co-signer with good credit significantly improves your chances of loan approval and can lead to more favorable terms. The co-signer assumes responsibility for the loan if you default. This is a significant commitment for the co-signer, so it’s crucial to have a transparent and honest conversation with them before involving them in the process. Choosing a reliable co-signer who understands the financial implications is essential.

Improving Credit Score

Improving your credit score is a long-term strategy but offers the most significant long-term benefits. By demonstrating responsible financial behavior, you can qualify for better loan terms in the future. This includes consistent on-time payments, maintaining low credit utilization, and avoiding new credit applications. A higher credit score translates directly to lower interest rates and more favorable loan terms.

Steps to Improve Financial Stability and Creditworthiness

Improving your financial stability and creditworthiness takes time and effort, but the payoff is well worth it. The following steps provide a roadmap to achieve better financial health:

- Pay all bills on time, every time. Even small, seemingly insignificant debts impact your credit score.

- Keep your credit utilization low (ideally below 30%). This refers to the amount of credit you’re using compared to your total available credit.

- Dispute any errors on your credit report. Incorrect information can negatively affect your score.

- Avoid opening multiple new credit accounts within a short period. Each application creates a hard inquiry, which can temporarily lower your score.

- Monitor your credit report regularly. Check for errors and track your progress over time. Services like AnnualCreditReport.com provide free access to your reports.

- Consider a secured credit card. This can help build credit history if used responsibly.

- Create and stick to a realistic budget. This helps you manage your finances effectively and avoid accumulating more debt.

Illustrative Scenarios

Understanding the realities of subprime auto lending requires examining specific scenarios. These examples illustrate the diverse outcomes borrowers can experience, highlighting the potential for both success and significant financial hardship. The scenarios presented are not exhaustive, but they offer a range of possibilities reflecting the complexities of the subprime lending market.

Successful Subprime Auto Loan Navigation

Maria, a single mother with a 500 credit score, needed a reliable car for her job and childcare responsibilities. She secured a subprime auto loan with a higher interest rate than prime borrowers would receive. However, she meticulously budgeted, prioritized loan payments, and avoided additional debt. By consistently making on-time payments, Maria demonstrated financial responsibility. Over time, her credit score gradually improved, allowing her to refinance at a lower interest rate and save money on future payments.

Her proactive approach and commitment to responsible financial management ultimately led to success.

Subprime Auto Loan Default

John, also with a 500 credit score, obtained a subprime auto loan for a used truck. He underestimated the financial burden of the higher interest rate and monthly payments. Facing unexpected job loss and mounting medical bills, John fell behind on his payments. The lender repossessed the truck, resulting in further damage to his credit score and potential legal repercussions.

This scenario highlights the vulnerability of borrowers with limited financial buffers when facing unforeseen circumstances.

Credit Score Improvement and Loan Refinancing, Subprime auto lenders for 500 credit score

After securing a subprime auto loan, Sarah diligently paid her monthly installments on time and paid down other debts. Over two years, she focused on improving her credit score by paying bills on time and reducing her credit utilization ratio. She consistently monitored her credit report for errors. This diligent effort resulted in a significant credit score increase. Sarah successfully refinanced her auto loan with a better interest rate and reduced monthly payment, significantly improving her financial situation.

Successful Exploration of Alternative Financing Options

David, needing a vehicle but wary of subprime loans, explored alternative financing options. He found a reputable buy-here-pay-here dealership willing to work with his credit history. While the interest rate was still higher than prime, it was more manageable than some subprime options. He also negotiated a reasonable down payment and payment schedule. By carefully selecting his vehicle and lender, David avoided the pitfalls of predatory subprime lenders and successfully secured transportation.

Visual Representation of Potential Financial Trajectories

Imagine a graph with “Time” on the x-axis and “Debt/Equity” on the y-axis. A line representing a negative trajectory starts high (representing the initial loan amount) and gradually increases due to high interest payments and potential late fees, eventually reaching a point where the debt significantly exceeds the vehicle’s value (repossession). A positive trajectory line starts at the same high point but gradually decreases as on-time payments are made, eventually reaching a point where the loan is paid off, representing a successful navigation of the subprime loan.

The difference between these lines vividly illustrates the impact of responsible financial management versus financial hardship.

Concluding Remarks

So, navigating the world of subprime auto loans with a 500 credit score definitely requires careful consideration. While it might seem daunting, understanding the risks, exploring all your options, and actively working to improve your credit score can significantly impact your success. Remember, responsible borrowing and smart financial planning are key to getting back on track, no matter where you start.

Don’t let a low credit score define your future; take control of your finances and drive towards a brighter tomorrow.