Refinance car loan to lower payments 2025? Totally doable! With interest rates fluctuating like a rollercoaster, now’s the time to see if refinancing your car loan can save you some serious cash. We’ll break down everything you need to know, from checking your credit score to comparing lenders and figuring out if it’s even worth it for your situation.

Get ready to ditch those high monthly payments and maybe even shorten your loan term!

This guide dives deep into the world of auto loan refinancing in 2025. We’ll explore current interest rates, eligibility requirements, the pros and cons, and the step-by-step process. We’ll even help you calculate potential savings and navigate the different refinancing options available. By the end, you’ll be equipped to make an informed decision about whether refinancing your car loan is the right move for you.

Current Interest Rates and Market Conditions in 2025

Auto loan interest rates in 2025 are a complex landscape shaped by various economic factors. Predicting exact numbers is impossible, but we can examine the likely trends and influencing variables to give you a clearer picture of what to expect when refinancing your car loan. Remember that these are estimates based on historical trends and current economic indicators; your individual rate will depend on your creditworthiness and the lender.

Thinking about refinancing your car loan in 2025 to lower your monthly payments? That’s smart! Lowering your expenses can free up cash for other things, like ensuring you have great car insurance coverage. Check out Top-rated car insurance companies for seniors 2025 to find the best deal for you, then get back to focusing on those sweet, sweet lower car payments.

Prevailing Interest Rate Environment for Auto Loans in 2025

The interest rate environment for auto loans in 2025 is projected to be moderately higher than the historically low rates seen in the previous decade, but still relatively manageable compared to some periods in the past. Several factors, such as inflation and the Federal Reserve’s monetary policy, will significantly influence the final numbers. While a specific percentage is difficult to predict, we can expect rates to fluctuate throughout the year, responding to changes in the overall economy.

Thinking about refinancing your car loan in 2025 to lower those monthly payments? It’s smart to consider all your car-related expenses, including insurance. Check out the average cost Average car insurance cost per month in Texas 2025 to get a better picture of your overall budget. Knowing this will help you determine how much lower your car payment needs to be to make a real difference in your finances.

For example, if inflation remains high, the Federal Reserve might raise interest rates further, impacting borrowing costs across the board, including auto loans. Conversely, if inflation cools down, rates could potentially stabilize or even slightly decrease.

Comparison of Interest Rates from Various Lenders

Different lenders offer varying interest rates on auto loans. Banks typically offer competitive rates, especially to customers with strong credit histories. Credit unions often provide slightly lower rates than banks due to their non-profit nature and focus on member benefits. Online lenders present a diverse range, with some offering highly competitive rates while others might charge higher rates to compensate for higher operational costs or riskier lending practices.

It’s crucial to compare offers from multiple lenders before making a decision. For instance, a large national bank might offer a slightly higher rate than a smaller regional bank but offer more flexible terms. Similarly, an online lender might offer a lower rate initially, but have stricter requirements or less customer service.

Factors Influencing Interest Rate Fluctuations

Several key factors contribute to the fluctuation of auto loan interest rates. The Federal Reserve’s monetary policy is a major player; changes in the federal funds rate directly affect the prime rate, which influences lending rates. Inflation rates also significantly impact interest rates. High inflation typically leads to higher interest rates as lenders adjust their rates to compensate for the decreased purchasing power of money.

Economic growth and unemployment rates also play a role; strong economic growth often leads to higher interest rates, while high unemployment can lead to lower rates. Finally, the demand for auto loans and the overall credit risk of borrowers affect the rates offered by lenders.

Average Interest Rates Across Different Credit Scores

The table below shows estimated average interest rates for new auto loans in 2025, categorized by credit score. These are broad averages and individual rates may vary based on the lender, loan term, and other factors.

| Credit Score Range | Average Interest Rate (Estimate) | Example Lender Type (Illustrative) | Potential Rate Variation |

|---|---|---|---|

| 750+ (Excellent) | 4.5% – 6.5% | Credit Union, National Bank | +/- 1% |

| 700-749 (Good) | 6% – 8% | Regional Bank, Online Lender | +/- 1.5% |

| 650-699 (Fair) | 8% – 10% | Online Lender, Smaller Banks | +/- 2% |

| Below 650 (Poor) | 10% + | Specialized Lenders, Buy-Here-Pay-Here Dealerships | +/- 3% or more |

Eligibility Criteria for Refinancing

So, you’re thinking about refinancing your car loan in 2025 to snag lower monthly payments? That’s smart! But before you start dreaming of extra cash, you need to understand what lenders look for. Getting approved hinges on several key factors, and meeting the criteria significantly increases your chances of success.Getting your car loan refinanced isn’t just about finding a better rate; it’s about proving to lenders you’re a responsible borrower.

Lenders assess your financial health to determine your risk level. This involves a careful review of your credit history, income, and the value of your car.

Credit Score Requirements

A strong credit score is your best friend when it comes to refinancing. Lenders generally prefer applicants with a credit score of at least 660, although some may consider applicants with scores as low as The higher your score, the better your chances of securing a favorable interest rate and terms. Think of it this way: a 750 credit score might get you a significantly lower interest rate than a 660 score, potentially saving you thousands over the life of the loan.

Conversely, a credit score below 620 might result in rejection or significantly less favorable terms.

Loan-to-Value Ratio (LTV)

Your loan-to-value ratio is the amount you owe on your car compared to its current market value. A lower LTV is generally preferred by lenders. For example, if your car is worth $20,000 and you owe $15,000, your LTV is 75%. A lower LTV (say, 60% or less) suggests less risk for the lender, making you a more attractive candidate for refinancing.

Lenders often set maximum LTV ratios for refinancing, and exceeding that limit can lead to denial.

Reasons for Refinancing Denial

Several scenarios can lead to a refinancing application being denied. These include: a low credit score (below the lender’s minimum threshold), a high loan-to-value ratio, a history of missed loan payments, insufficient income to support the new loan payments, the car being too old or having excessive mileage (lenders often have age and mileage limits), or an existing loan that is already in default.

For instance, if you’ve recently experienced bankruptcy or foreclosure, refinancing might be challenging. Similarly, if your car is significantly depreciated, making your LTV too high, your application might be rejected.

Benefits of Refinancing a Car Loan

Refinancing your car loan in 2025 could offer significant financial advantages, especially considering the fluctuating interest rate environment. By strategically refinancing, you can potentially save money, improve your financial situation, and even boost your credit score. Let’s explore the key benefits.Lower Monthly Payments and Shorter Loan Terms are two major draws of refinancing. These benefits are directly tied to securing a lower interest rate than your current loan.

This can free up cash flow for other financial goals or simply provide more breathing room in your monthly budget. Furthermore, refinancing can allow you to shorten the loan term, leading to less interest paid over the life of the loan.

Lower Monthly Payments

Lower monthly payments are arguably the most attractive benefit of refinancing. Imagine you’re currently paying $500 a month on a car loan with a high interest rate. By refinancing, you might be able to lower that payment to $400, freeing up $100 each month. That extra $100 could go towards paying down other debts, saving for a down payment on a house, or simply enjoying more disposable income.

The actual savings will depend on the new interest rate you qualify for and the length of the new loan term. For example, refinancing a $20,000 loan from 8% interest to 5% interest over 60 months could result in monthly savings of approximately $60-$80, depending on the specific loan terms.

Shorter Loan Term

Refinancing also presents the opportunity to shorten your loan term. While this might mean slightly higher monthly payments, it ultimately leads to significant long-term savings on interest. Let’s say you have a 72-month loan. Refinancing to a 48-month loan, even with a slightly higher monthly payment, will drastically reduce the total interest you pay over the life of the loan.

This is because you’re paying off the principal faster, minimizing the amount of interest accrued. A shorter loan term also means you own your car outright sooner.

Improved Credit Score

While not always guaranteed, successfully refinancing your car loan can positively impact your credit score. A lower debt-to-income ratio, resulting from lower monthly payments or a shorter loan term, can improve your creditworthiness. On the other hand, a missed payment during the refinancing process or taking on more debt simultaneously could negatively affect your score. Therefore, responsible financial management is crucial throughout the refinancing process.

Responsible credit management consistently demonstrates financial responsibility to credit bureaus.

Additional Benefits

Beyond lower payments and a shorter loan term, refinancing can offer other advantages. For example, it can simplify your finances by consolidating multiple auto loans into a single, easier-to-manage payment. It can also provide peace of mind, knowing you’re paying a lower interest rate and are on a more manageable repayment schedule. This can be especially beneficial if interest rates have dropped significantly since you originally took out your loan.

- Reduced monthly payments, freeing up cash flow.

- Shorter loan term, resulting in less interest paid overall.

- Potential improvement in credit score due to a lower debt-to-income ratio.

- Simplified finances through loan consolidation.

- Increased financial peace of mind with a more manageable repayment plan.

Potential Drawbacks of Refinancing

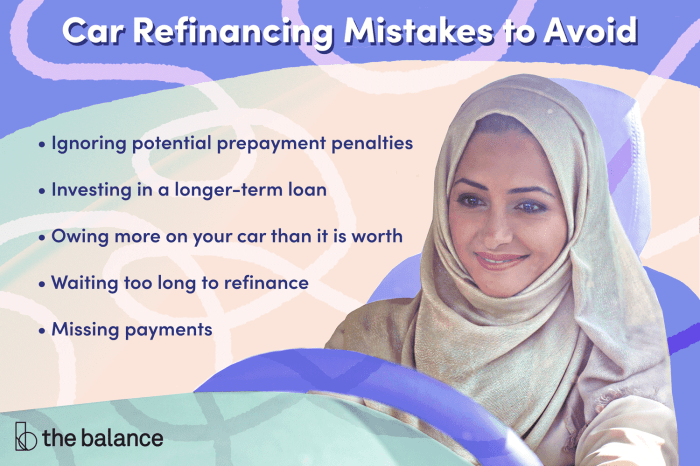

Refinancing your car loan might seem like a no-brainer to lower your monthly payments, but it’s crucial to weigh the potential downsides before you sign on the dotted line. While a lower monthly payment can be tempting, it’s important to understand how refinancing could impact your overall cost and financial situation. Failing to consider these factors could lead to unexpected expenses and a less-than-ideal outcome.

One significant drawback is the possibility of paying more interest overall. A longer loan term, often a key feature of refinancing for lower payments, means you’ll be paying interest for a longer period. While your monthly payments decrease, the total interest paid over the life of the loan will likely increase. This increase can significantly outweigh the benefits of lower monthly payments, especially if you plan to pay off the loan early.

Prepayment Penalties

Prepayment penalties are fees charged by lenders if you pay off your loan before the agreed-upon term. These penalties can be substantial, potentially negating any savings achieved through refinancing. Before refinancing, carefully review the terms of your current and potential new loan agreements to determine if prepayment penalties apply and how much they might cost. If you anticipate paying off your loan early, refinancing might not be the best option.

Situations Where Refinancing Might Not Be Beneficial

Refinancing isn’t always the best financial move. For instance, if you have a short time left on your current loan, the potential savings from refinancing might not be worth the hassle and fees. Similarly, if interest rates have risen significantly since you took out your original loan, refinancing could result in a higher interest rate, increasing your overall cost.

Additionally, if your credit score has declined since your initial loan, you may not qualify for a better interest rate, rendering refinancing pointless. A thorough cost-benefit analysis is crucial before proceeding.

Comparison of Total Interest Paid Under Different Refinancing Scenarios

The following table illustrates how total interest paid can vary depending on the loan term and interest rate. These are hypothetical examples and actual results may differ.

| Scenario | Original Loan Term (Years) | Original Interest Rate (%) | Refinanced Loan Term (Years) | Refinanced Interest Rate (%) | Total Interest Paid |

|---|---|---|---|---|---|

| Original Loan | 4 | 6 | – | – | $1,500 (example) |

| Refinance 1 (Longer Term) | 4 | 6 | 6 | 5.5 | $2,200 (example) |

| Refinance 2 (Shorter Term, Higher Rate) | 4 | 6 | 3 | 7 | $1,800 (example) |

Steps Involved in the Refinancing Process

Refinancing your car loan can seem daunting, but breaking it down into manageable steps makes the process much less stressful. Think of it like a well-organized road trip – you need a plan, the right tools, and a little patience to reach your destination (lower monthly payments!). This section will walk you through each stage, from initial research to securing your new loan.

Application for Car Loan Refinancing

The application process typically begins online or at a lender’s physical location. You’ll start by providing some basic information about yourself and your current car loan. Many lenders offer pre-qualification tools which allow you to check your eligibility without impacting your credit score. This is a great way to get a feel for what rates and terms you might qualify for before formally applying.

After pre-qualification, you’ll submit a full application, providing more detailed financial information. This often involves completing an online form and uploading supporting documents.

Comparing Different Loan Offers

Once you’ve applied to a few lenders, you’ll likely receive multiple loan offers. It’s crucial to compare these offers carefully before making a decision. Don’t just focus on the monthly payment; consider the total interest paid over the life of the loan (the total cost), the loan term (length of the loan), and the Annual Percentage Rate (APR).

A lower monthly payment might seem appealing, but a longer loan term could mean paying significantly more interest in the long run. Creating a simple comparison table, listing each lender’s APR, monthly payment, loan term, and total interest paid, will help you visualize the differences and make an informed choice. For example, Lender A might offer a lower monthly payment but a higher APR and longer term, resulting in a higher total interest cost compared to Lender B.

Documentation Needed for Refinancing

Lenders require specific documentation to verify your income, creditworthiness, and the details of your current car loan. This typically includes: your driver’s license or state-issued ID, proof of income (pay stubs, tax returns, or bank statements), your current car loan details (loan agreement, payoff amount), your vehicle’s title (or proof of ownership), and your credit report (often obtained by the lender).

Having these documents readily available will streamline the application process and expedite approval. Failing to provide necessary documentation can lead to delays.

Flowchart Illustrating the Refinancing Process

Imagine a flowchart with several boxes connected by arrows.The first box: “Initiate Refinancing Research.” This leads to two boxes: “Check Eligibility/Pre-qualification” and “Gather Necessary Documents.” “Check Eligibility/Pre-qualification” leads to “Apply to Multiple Lenders.” “Gather Necessary Documents” connects to “Apply to Multiple Lenders” as well. “Apply to Multiple Lenders” leads to “Compare Loan Offers.” “Compare Loan Offers” leads to “Select Best Offer and Sign Documents.” Finally, “Select Best Offer and Sign Documents” leads to “Loan Funding and Payoff of Existing Loan.” This visual representation helps to understand the sequential nature of the process.

Comparison of Different Refinancing Options

Choosing the right refinance option can significantly impact your monthly payments and overall loan cost. Several factors need careful consideration, including the lender, loan type, and loan term. This section will compare and contrast various refinancing options to help you make an informed decision.

Lender Comparison: Banks, Credit Unions, and Online Lenders, Refinance car loan to lower payments 2025

Different lenders offer varying interest rates, fees, and loan terms. Banks typically offer a wide range of products but may have stricter eligibility requirements and higher fees. Credit unions often provide more competitive rates and personalized service to their members, but membership may be required. Online lenders are known for their convenience and potentially lower rates due to reduced overhead, but they may lack the personalized touch of traditional lenders.

For example, a major bank might offer a 6.5% APR refinance loan with a $500 origination fee, while a credit union might offer 6% APR with a $250 fee, and an online lender might advertise a 5.8% APR with no origination fee but a slightly higher monthly payment due to a shorter loan term. These differences highlight the importance of comparing offers across various lenders before making a decision.

Fixed-Rate vs. Variable-Rate Loans

Fixed-rate loans offer predictable monthly payments because the interest rate remains constant throughout the loan term. This stability makes budgeting easier. Variable-rate loans, on the other hand, have an interest rate that fluctuates based on market conditions. While they might start with a lower rate than a fixed-rate loan, the rate could increase over time, leading to higher monthly payments.

Consider your risk tolerance and financial predictability needs when deciding between these two options. A fixed-rate loan provides certainty, while a variable-rate loan offers the potential for lower initial payments but carries the risk of increased payments if interest rates rise.

Implications of Different Loan Terms

The length of your loan, or loan term, directly impacts your monthly payment and total interest paid. A shorter loan term means higher monthly payments but less interest paid over the life of the loan. Conversely, a longer loan term results in lower monthly payments but higher total interest paid. For example, refinancing a $20,000 loan at 6% APR for 36 months results in higher monthly payments than a 60-month loan term, but you’ll pay significantly less interest overall with the shorter term.

Choosing the right term involves balancing affordability with the long-term cost of the loan.

Examples of Loan Offers

Let’s consider three hypothetical loan offers for a $25,000 refinance:

| Lender | Interest Rate (APR) | Loan Term (Months) | Monthly Payment (approx.) | Total Interest Paid (approx.) |

|---|---|---|---|---|

| National Bank | 7.0% | 60 | $500 | $4,000 |

| Local Credit Union | 6.5% | 48 | $580 | $3,200 |

| Online Lender | 6.0% | 36 | $760 | $2,160 |

These examples illustrate how interest rates and loan terms interact to influence monthly payments and total interest costs. The online lender offers the lowest interest rate, resulting in the lowest total interest paid, but this comes with a substantially higher monthly payment. The credit union offers a balance between interest and monthly payments. The bank offers the lowest monthly payment but the highest total interest.

The “best” option depends entirely on individual financial priorities and circumstances.

Calculating Potential Savings

Refinancing your car loan can lead to significant savings, but understanding how to calculate those savings is key to making an informed decision. This section will Artikel the methods for calculating potential monthly payment reductions and total interest saved, providing you with the tools to assess the financial benefits of refinancing.

The most straightforward way to determine potential savings involves comparing your current monthly payment with the projected monthly payment after refinancing. This comparison highlights the immediate financial impact of refinancing.

Monthly Payment Savings Calculation

To calculate your potential monthly payment savings, you need to know your current monthly payment and your projected monthly payment after refinancing. The formula is simple:

Monthly Savings = Current Monthly Payment – New Monthly Payment

Let’s illustrate with an example. Suppose your current monthly payment is $500, and after refinancing, your new monthly payment is projected to be $400. Your monthly savings would be $500 – $400 = $100.

Total Interest Saved Calculation

Calculating the total interest saved requires a bit more work. You need to determine the total interest paid under your current loan and the total interest paid under the refinanced loan. The difference represents your total interest savings.

Total Interest Saved = Total Interest Paid (Current Loan)

Total Interest Paid (Refinanced Loan)

This calculation often requires using a loan amortization calculator available online or through your lender. Inputting your loan details (principal, interest rate, and loan term) will provide the total interest paid for each scenario. For instance, let’s assume the total interest paid on your current loan is $5,000, and after refinancing, it’s projected to be $3,000. Your total interest savings would then be $5,000 – $3,000 = $2,000.

Potential Savings Under Different Scenarios

The following table illustrates potential savings under various scenarios, assuming a current loan of $20,000. Note that these are illustrative examples and actual savings will vary based on individual circumstances and market conditions.

| Current Interest Rate | New Interest Rate | Loan Term (Years) | Monthly Savings |

|---|---|---|---|

| 7% | 5% | 60 | $75 |

| 7% | 4% | 60 | $100 |

| 7% | 5% | 48 | $50 |

| 9% | 6% | 60 | $80 |

Factors to Consider Before Refinancing: Refinance Car Loan To Lower Payments 2025

Refinancing your car loan can seem like a no-brainer if you’re offered a lower interest rate, but it’s crucial to carefully weigh the pros and cons before diving in. A hasty decision could end up costing you more in the long run. Take the time to analyze your financial situation and the terms of the new loan to ensure it’s the right move for you.Considering all aspects before refinancing is crucial for making a financially sound decision.

Failing to do so could lead to unforeseen consequences, potentially negating the benefits of a lower monthly payment. Thorough research and planning are key to a successful refinance.

Loan Agreement Review

Before signing anything, meticulously review the terms of your current auto loan and the proposed refinance agreement. Pay close attention to the interest rate (both APR and simple interest), loan term length, any prepayment penalties, and additional fees. Compare these details side-by-side to understand the true cost of refinancing. For example, a slightly lower interest rate might be offset by a longer loan term, ultimately increasing the total interest paid over the life of the loan.

A seemingly attractive offer might not be as beneficial as it initially appears.

Implications of Changing Lenders

Switching lenders involves more than just a new interest rate. You’ll need to consider the lender’s reputation, customer service, and the ease of making payments. Some lenders offer online portals for easy payment tracking and management, while others might require manual payments through mail or in-person visits. A less convenient payment process could offset any savings achieved through refinancing.

Additionally, transferring your loan might involve some administrative hassle and potential delays. For instance, you might experience a short period where payments are temporarily suspended while the transfer is processed.

Refinancing Checklist

Before you initiate the refinancing process, use this checklist to ensure you’ve considered all the key factors:

- Current Loan Details: Review your current interest rate, loan term, remaining balance, and any prepayment penalties.

- New Loan Offers: Compare multiple offers from different lenders, focusing on APR, loan term, and fees.

- Credit Score Impact: Understand that applying for a new loan will result in a hard inquiry on your credit report, which can temporarily lower your score.

- Financial Situation: Assess your current financial stability and ability to consistently make payments under the new loan terms.

- Total Interest Paid: Calculate the total interest you’ll pay under both your current loan and the proposed refinance. Don’t just focus on the monthly payment reduction.

- Lender Reputation: Research the reputation and customer service of any lender you’re considering.

- Payment Method Convenience: Consider the convenience of the payment methods offered by the new lender.

Wrap-Up

So, should you refinance your car loan in 2025? The answer depends entirely on your individual financial situation and goals. By carefully considering the factors we’ve Artikeld – interest rates, eligibility, potential savings, and potential drawbacks – you can make a smart, informed decision. Remember to shop around, compare offers, and read the fine print before signing anything.

Lower payments and a brighter financial future await!