New Jersey auto insurance requirements 2025 are shaping up to be a pretty big deal for Garden State drivers. Understanding these rules isn’t just about avoiding a ticket; it’s about protecting yourself financially if you’re in an accident. This guide breaks down the key changes and what you need to know to stay covered and avoid any nasty surprises.

From minimum coverage limits for liability and uninsured/underinsured motorists to the ins and outs of Personal Injury Protection (PIP) and how your driving record impacts your premiums, we’ll cover it all. We’ll even give you some tips on filing a claim and resolving disputes with your insurance company. Get ready to become a New Jersey auto insurance pro!

Minimum Coverage Requirements in New Jersey for 2025

New Jersey has minimum auto insurance requirements that all drivers must meet. These requirements ensure a basic level of financial protection for individuals injured or whose property is damaged in accidents. Understanding these minimums is crucial for responsible driving and avoiding potential financial ruin. Failure to carry the required minimum insurance can result in significant penalties.

For 2025, New Jersey’s minimum auto insurance coverage requirements remain the same as in previous years. These requirements are designed to compensate victims of car accidents for their medical bills and property damage. It’s important to remember that these are minimums, and carrying higher coverage limits offers significantly greater protection.

Bodily Injury Liability Coverage

Bodily injury liability coverage pays for the medical expenses, lost wages, and pain and suffering of individuals injured in an accident you caused. In New Jersey, the minimum requirement for bodily injury liability is 15/30. This means $15,000 per person injured and $30,000 total per accident. For example, if you cause an accident injuring two people, the maximum your insurance will pay is $30,000, even if one person’s medical bills exceed $15,000.

Property Damage Liability Coverage

Property damage liability coverage pays for the cost of repairing or replacing damaged property, such as another person’s vehicle, in an accident you caused. The minimum requirement in New Jersey is $15,000. This means your insurance will pay a maximum of $15,000 for damage to another person’s property. If the damage exceeds this amount, you would be personally responsible for the difference.

Examples of Insufficient Minimum Coverage

Consider these scenarios: You cause an accident injuring three people. One suffers severe injuries resulting in $20,000 in medical bills, another has $10,000 in bills, and the third has $5,000. Your minimum coverage of $30,000 is insufficient to cover the total medical bills of $35,000. You would be personally liable for the remaining $5,000. Similarly, if you cause an accident that totals a luxury vehicle with $25,000 in damages, your $15,000 property damage liability coverage would leave you responsible for $10,000.

Comparison of Minimum Coverage Requirements

Comparing New Jersey’s minimum coverage to neighboring states highlights the variations in legal protection. The following table shows the differences.

| State | Bodily Injury (per person) | Bodily Injury (per accident) | Property Damage |

|---|---|---|---|

| New Jersey | $15,000 | $30,000 | $15,000 |

| New York | $25,000 | $50,000 | $10,000 |

| Pennsylvania | $15,000 | $30,000 | $5,000 |

| Delaware | $25,000 | $50,000 | $25,000 |

Uninsured/Underinsured Motorist Coverage in NJ 2025

Protecting yourself on New Jersey roads means understanding the risks, and a significant one is the high number of uninsured drivers. UM/UIM coverage is your safety net in the event you’re hit by someone without adequate insurance or who is underinsured. It’s a crucial addition to your basic auto insurance policy, providing financial protection when you need it most.UM/UIM coverage steps in when you’re injured in an accident caused by an uninsured or underinsured driver.

This coverage is separate from your liability coverage, which pays for damages you cause to others. Instead, UM/UIM covers your medical bills, lost wages, and property damage if you’re hurt by a driver who doesn’t have enough insurance to cover your losses. It’s a vital layer of protection, especially considering the significant number of uninsured motorists on New Jersey roads.

Types of UM/UIM Coverage

UM/UIM coverage comes in two main forms: bodily injury and property damage. Bodily injury coverage protects you and your passengers for medical expenses, lost wages, and pain and suffering resulting from an accident with an uninsured or underinsured driver. Property damage coverage protects your vehicle against damage caused by an uninsured or underinsured driver. You can choose separate limits for each type of coverage.

It’s important to select limits that reflect the potential costs associated with serious injuries and vehicle repairs.

Hypothetical Scenario Illustrating UM/UIM Coverage Benefits

Imagine you’re driving home from work one evening. A car runs a red light and T-bones your vehicle. You sustain significant injuries requiring extensive medical treatment and physical therapy. The other driver is uninsured. Without UM/UIM coverage, you’re responsible for all your medical bills, lost wages, and other expenses.

However, with UM/UIM coverage, your own insurance company will step in to cover these costs, up to your policy limits. This can mean the difference between financial ruin and recovery after a serious accident. The peace of mind provided by knowing you have this coverage is invaluable.

Personal Injury Protection (PIP) in New Jersey for 2025

PIP coverage in New Jersey is a crucial part of your auto insurance policy. It’s designed to protect you and your passengers, regardless of who’s at fault in an accident. Essentially, it acts as a safety net, covering medical bills and other expenses, even if you’re injured in a crash caused by your own mistake. Understanding its function is key to choosing the right coverage for your needs.PIP coverage in New Jersey helps pay for a range of expenses related to injuries sustained in a car accident.

This includes medical bills, such as doctor visits, hospital stays, surgery, physical therapy, and prescription medications. It also covers lost wages if your injuries prevent you from working, as well as other expenses like funeral costs in the case of a fatality. The specific benefits covered and the limits on those benefits are determined by the level of PIP coverage you select.

PIP Coverage Limits and Their Implications, New Jersey auto insurance requirements 2025

Choosing a lower PIP coverage limit means you’ll have less financial protection in the event of a serious accident. For example, a low limit might only cover a portion of your medical bills, leaving you responsible for significant out-of-pocket expenses. Consider a scenario where you’re involved in a severe accident requiring extensive rehabilitation. A low PIP limit could quickly become insufficient to cover the costs of treatment and lost income, potentially leading to substantial personal financial strain.

Higher limits offer greater peace of mind, knowing that a wider range of expenses will be covered.

PIP Coverage versus Health Insurance

While both PIP and health insurance cover medical expenses, they function differently. Health insurance typically requires you to meet a deductible and co-pays, while PIP coverage often pays benefits directly to the healthcare provider, without the need for upfront payments from you. Furthermore, health insurance might not cover all the expenses related to a car accident, such as lost wages.

PIP specifically addresses these accident-related expenses, supplementing your health insurance. It’s important to note that some health insurance plans may have clauses that limit coverage for injuries received in a car accident, making PIP even more important. In essence, PIP and health insurance are complementary forms of coverage; they work together to provide a more comprehensive financial safety net in the aftermath of a car accident.

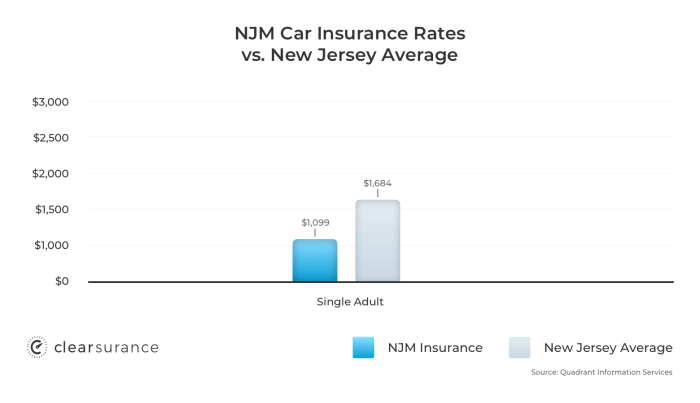

Factors Affecting New Jersey Auto Insurance Premiums in 2025

So, you’re trying to figure out why your car insurance in New Jersey costs what it does? It’s not just a random number; several factors go into determining your premium. Understanding these factors can help you make informed decisions to potentially lower your costs. Let’s dive into the key elements influencing your 2025 New Jersey auto insurance rates.

Several interconnected elements contribute to the final price of your New Jersey auto insurance. These factors are often weighted differently depending on the individual and their insurance company, but understanding their impact is crucial for cost management.

Figuring out New Jersey auto insurance requirements for 2025 can be a total headache, especially if you’re a student. To make things easier, check out this helpful resource on finding the Best car insurance for college students 2025 to help navigate the process. Once you’ve got that sorted, you’ll be much better prepared to meet all those pesky NJ insurance rules.

Driving Record

Your driving history is arguably the most significant factor influencing your premium. Insurance companies assess your risk based on past accidents, traffic violations, and even the number of years you’ve been driving. A clean driving record translates to lower premiums, reflecting a lower perceived risk. Conversely, accidents and tickets, especially serious ones like DUIs, significantly increase your premiums.

For example, a driver with three speeding tickets in the past three years will likely pay considerably more than a driver with a spotless record. Similarly, being involved in an at-fault accident can result in a premium increase for several years.

Vehicle Type

The type of car you drive plays a substantial role in your insurance costs. Insurance companies consider factors like the vehicle’s make, model, year, safety features, and repair costs. Generally, expensive cars with high repair costs command higher premiums due to the greater potential financial liability for the insurer.

So, New Jersey’s auto insurance requirements in 2025 are pretty strict, right? If you’re looking to save some serious cash, you might want to check out the Cheapest states for car insurance in 2025 to see if a move is worth it. Of course, that depends on how much you value those NJ benefits and whether the savings outweigh the hassle.

Ultimately, figuring out your New Jersey 2025 insurance needs is key.

A high-performance sports car will typically be more expensive to insure than a smaller, economical sedan. This is because sports cars are often involved in more severe accidents and have higher repair costs. Conversely, cars with advanced safety features like automatic emergency braking may qualify for discounts.

Location

Where you live in New Jersey significantly impacts your insurance rates. Areas with higher rates of accidents and theft generally have higher insurance premiums. This is because insurance companies assess the risk of insuring vehicles in high-risk areas.

Living in a densely populated urban area with a high crime rate will likely result in higher premiums compared to residing in a rural area with lower accident statistics. Insurance companies use statistical data on accident frequency and severity within specific zip codes to calculate risk.

Age and Driving Experience

Your age and driving experience are also key factors. Younger drivers, especially those with less than three years of driving experience, are statistically more likely to be involved in accidents, leading to higher premiums. As you gain experience and age, your premiums typically decrease.

A teenager with a learner’s permit will pay significantly more than a seasoned driver with a decade of accident-free driving. This reflects the increased risk associated with inexperienced drivers. As drivers reach their mid-thirties and beyond, premiums often level off or even decrease.

Credit Score

In New Jersey, your credit score can influence your auto insurance premium. While controversial, many insurers believe that a good credit score reflects responsible financial behavior, which can be correlated with responsible driving. Therefore, drivers with good credit scores often receive lower premiums.

While not directly related to driving ability, a poor credit score can lead to higher premiums, sometimes significantly. This is because insurers view a poor credit score as an indicator of higher risk. Improving your credit score can be a way to potentially lower your auto insurance costs.

Filing an Auto Insurance Claim in New Jersey (2025)

Filing an auto insurance claim in New Jersey can seem daunting, but a methodical approach simplifies the process. Understanding the steps involved and gathering necessary information promptly will significantly expedite your claim’s resolution. Remember, prompt action is key.

Steps to File an Auto Insurance Claim in New Jersey

After a car accident in New Jersey, immediately prioritize safety. Check for injuries and call emergency services if needed. Then, focus on documenting the accident and initiating the claims process.

- Secure the Scene: If possible and safe, move vehicles to a location that minimizes further risk. Turn on hazard lights.

- Contact Emergency Services: Call 911 if anyone is injured or if the accident involves significant property damage. Obtain a police report number if one is generated.

- Exchange Information: Gather contact and insurance information from all involved parties, including drivers, passengers, and witnesses. Note down license plate numbers, vehicle makes and models, and insurance company names.

- Document the Accident: Take photographs or videos of the accident scene, including damage to vehicles, visible injuries, and road conditions. Note the time, date, and location of the accident. Obtain contact information from any witnesses.

- Contact Your Insurance Company: Report the accident to your insurance company as soon as possible, usually within 24-48 hours. Provide them with all the information you gathered.

- Seek Medical Attention: Even if you feel fine, seek medical attention promptly. Delayed reporting of injuries can complicate your claim.

- Cooperate with the Investigation: Your insurance company may request additional information or documentation. Cooperate fully and respond promptly to their requests.

- Keep Records: Maintain meticulous records of all communication, documentation, medical bills, repair estimates, and other relevant expenses related to the accident.

Claim Process Flowchart

The following flowchart visually represents the typical steps involved in the claim process.

| Step | Action | Outcome | Next Step |

|---|---|---|---|

| 1 | Accident Occurs | Injury/Damage | 2 |

| 2 | Call Emergency Services & Exchange Information | Police Report (Optional), Contact Information | 3 |

| 3 | Document the Accident (Photos, Videos) | Visual Record of the Scene | 4 |

| 4 | Contact Your Insurance Company | Claim Filed | 5 |

| 5 | Insurance Investigation | Claim Approved/Denied/Further Investigation Needed | 6 |

| 6 | Settlement Negotiations (if Approved) | Agreement Reached | 7 |

| 7 | Claim Settlement/Payment | Claim Resolved | – |

Dispute Resolution in New Jersey Auto Insurance Claims

Navigating a disagreement with your auto insurance company can be stressful, but New Jersey offers several avenues for resolving disputes fairly. Understanding these options can empower you to advocate for your rights and secure a just settlement. This section Artikels the process for resolving insurance claim disputes in New Jersey, including mediation and arbitration, and clarifies the role of the state’s Department of Banking and Insurance.Disputes with your insurance company often arise from disagreements over the amount of coverage, the cause of an accident, or the assessment of damages.

Before resorting to formal dispute resolution, it’s crucial to thoroughly document your claim, including all relevant communication with your insurer. Keeping records of phone calls, emails, and letters is essential. Attempting to resolve the issue directly with your insurer through clear and concise communication is the first step. If this fails, you have several options.

Mediation as a Dispute Resolution Method

Mediation involves a neutral third party, a mediator, who facilitates communication between you and your insurance company. The mediator doesn’t make a decision; instead, they help both sides understand each other’s perspectives and work towards a mutually agreeable solution. Mediation is often less expensive and time-consuming than arbitration or litigation. The mediator guides the discussion, helping to identify common ground and explore potential compromises.

A successful mediation results in a written agreement that is legally binding. For example, a disagreement over the value of a damaged vehicle might be resolved through mediation, resulting in a settlement that’s acceptable to both parties.

Arbitration as a Dispute Resolution Method

Arbitration is a more formal process than mediation. Here, a neutral arbitrator hears evidence and arguments from both sides and then renders a binding decision. This decision is legally enforceable, much like a court judgment. Arbitration is often chosen when mediation fails to resolve the dispute. The arbitrator’s decision is final and can address the specific points of contention, such as the amount of property damage or the extent of medical expenses covered.

For instance, a dispute over the extent of injuries sustained in an accident could be settled through arbitration, where the arbitrator would review medical records and testimony to determine the appropriate compensation.

The Role of the New Jersey Department of Banking and Insurance

The New Jersey Department of Banking and Insurance (DOBI) plays a crucial role in overseeing the insurance industry and resolving disputes. They investigate complaints against insurance companies and can take enforcement action if necessary. Consumers can file complaints with the DOBI if they believe their insurer has acted unfairly or in bad faith. The DOBI can mediate disputes, conduct investigations, and even impose penalties on insurers who violate state regulations.

This provides a valuable avenue for recourse if informal attempts at dispute resolution have proven unsuccessful. For example, if an insurer refuses to pay a legitimate claim based on unsubstantiated reasons, the DOBI can intervene to protect the policyholder’s rights.

New Jersey’s Point System and its Impact on Insurance Rates: New Jersey Auto Insurance Requirements 2025

New Jersey utilizes a point system to track driving violations, directly impacting your auto insurance premiums. Essentially, each violation earns you points, and accumulating too many points can significantly increase your insurance costs. Insurance companies use this system to assess risk, meaning a driver with more points is considered a higher risk and therefore charged more.The more points you accumulate, the higher your insurance rates will climb.

This is because a higher point total indicates a greater likelihood of future accidents or violations. Insurance companies are in the business of managing risk, and they use the point system as a key factor in determining your premium. Think of it like this: a driver with a clean record is a low-risk driver, while a driver with multiple violations is a high-risk driver, hence the increased cost.

Point Values for Driving Violations

The number of points assigned to a violation depends on its severity. Minor offenses like speeding slightly over the limit might only add a few points, while more serious offenses like driving under the influence (DUI) or reckless driving will result in a substantial increase. These points stay on your driving record for a specific period, usually three to five years, depending on the violation.

This timeframe impacts how long the increased premiums persist.

- Speeding (1-15 mph over): Typically 2 points. This could vary slightly depending on the specific speed and location.

- Speeding (16-29 mph over): Typically 4 points. Again, location and specific speed can affect the exact point value.

- Driving While Intoxicated (DWI): This results in a significant number of points, often 12 points or more. The exact number can depend on factors like blood alcohol content (BAC) and other circumstances.

- Reckless Driving: Usually results in 5 points or more, reflecting the serious nature of the offense.

- Failure to Yield: Typically receives 2 points, highlighting the importance of safe driving practices.

Impact of Accumulated Points on Insurance Premiums

The effect of accumulated points on insurance premiums is not linear. Meaning, two points don’t necessarily double the increase compared to one point. Instead, the impact tends to be more substantial as the number of points increases. Insurance companies have complex algorithms that consider various factors, including the number of points, the type of violations, and the driver’s history.For example, a driver with 2 points might see a modest increase in their premium, perhaps 10-15%.

However, a driver with 8 points could face a premium increase of 50% or even more, depending on the insurer and other individual factors. A driver with a history of multiple serious violations could find their insurance significantly more expensive or even face difficulty obtaining coverage. In some cases, insurers may cancel policies for drivers with an excessive number of points.

Resources for New Jersey Drivers Regarding Auto Insurance

Navigating the world of New Jersey auto insurance can be confusing, but thankfully, several resources are available to help drivers understand their rights and responsibilities. These resources offer valuable information on coverage options, claim procedures, and dispute resolution, empowering drivers to make informed decisions and protect themselves financially. Utilizing these resources can save you time, money, and stress.Finding reliable information is key to making smart choices about your auto insurance.

The following list provides access to official government agencies and trusted consumer advocacy organizations. These groups offer a range of services, from providing clear explanations of New Jersey’s insurance laws to assisting with resolving disputes with your insurance company.

Reputable Resources for New Jersey Auto Insurance Information

Accessing accurate and up-to-date information is crucial for making informed decisions about your auto insurance. The following list highlights key resources that provide comprehensive information and assistance to New Jersey drivers.

- New Jersey Department of Banking and Insurance: This state agency regulates the insurance industry in New Jersey and provides a wealth of information on insurance laws, consumer rights, and complaint procedures. Their website offers detailed guides, FAQs, and contact information for assistance.

- New Jersey Division of Consumer Affairs: This division works to protect consumers from unfair or deceptive business practices. They can help with filing complaints against insurance companies and provide resources on resolving insurance disputes.

- National Association of Insurance Commissioners (NAIC): The NAIC is an organization of state insurance regulators that works to promote consumer protection and fair insurance practices. Their website offers valuable information on insurance regulations and consumer rights across all states, including New Jersey.

- Consumer Reports: This non-profit organization provides independent reviews and ratings of various products and services, including auto insurance companies. Their research can help you compare different insurers and choose a policy that meets your needs and budget.

- Your Insurance Company’s Website: While not a neutral source, your insurance company’s website usually contains helpful information about your policy, coverage details, and claim filing procedures. It’s a good place to access your policy documents and find contact information for customer service.

Benefits of Utilizing Available Resources

Taking advantage of the resources listed above offers significant benefits to New Jersey drivers. By accessing reliable information and utilizing available assistance programs, drivers can ensure they understand their policy, file claims effectively, and resolve disputes fairly. This proactive approach can save both time and money in the long run. These resources empower consumers to navigate the complexities of auto insurance with confidence and make informed decisions that best protect their interests.

Closing Notes

Navigating New Jersey’s auto insurance landscape can feel like driving through rush hour traffic, but with a little knowledge, it doesn’t have to be a headache. By understanding the minimum coverage requirements, the importance of UM/UIM coverage, and the factors influencing your premiums, you can make informed decisions to protect yourself and your wallet. Remember to always review your policy and reach out to your insurer or the state’s Department of Banking and Insurance if you have any questions.

Stay safe out there, Jersey drivers!