Gap insurance for financed cars 2025? Yeah, it’s a total lifesaver if you’re financing a ride. Basically, it covers the difference between what you owe on your loan and what your car is worth after an accident – a huge gap that can leave you seriously in debt. This isn’t your grandma’s insurance; we’re diving into the nitty-gritty of how it works, how much it costs, and whether it’s worth the extra cash in 2025.

We’ll break down everything from choosing a provider (dealership vs. independent) to understanding those sneaky hidden fees. Think of it as your ultimate guide to navigating the world of gap insurance and making sure you’re not left holding the bag after a fender bender (or worse!). We’ll also look at how the changing car market and loan options are affecting gap insurance in 2025 and beyond.

Understanding Gap Insurance in 2025

Gap insurance is a smart financial move for anyone financing a car. It bridges the gap between what you owe on your loan and what your car is worth after an accident or theft. Essentially, it protects you from being on the hook for thousands of dollars if your car is totaled and its value is less than your loan balance.Gap insurance protects car owners from significant financial losses after a total loss accident or theft.

Standard auto insurance typically covers the actual cash value (ACV) of your vehicle. However, if you’re still paying off a car loan, the ACV might be significantly lower than the amount you owe. Gap insurance steps in to cover that difference, preventing you from having to pay off the remaining loan balance out of pocket.

Gap Insurance Compared to Other Auto Insurance

Gap insurance isn’t a replacement for comprehensive or collision coverage; it worksin addition* to your standard auto insurance. Comprehensive coverage handles damage from events like fire, theft, or vandalism, while collision coverage takes care of damage from accidents. Think of gap insurance as a supplemental policy that specifically addresses the loan balance shortfall after a total loss. It doesn’t cover repairs or smaller accidents; its sole purpose is to cover the difference between your car’s value and what you owe.

So, you’re looking at Gap insurance for financed cars in 2025? That’s smart, especially if you’re upside down on your loan. Finding the right coverage can be tricky, and it’s also a good idea to compare rates for your overall auto insurance, which is why checking out resources like Cheapest car insurance in Michigan no-fault 2025 might be helpful, especially if you’re in Michigan.

Ultimately, securing the best Gap insurance depends on your individual needs and financial situation.

Situations Where Gap Insurance is Most Beneficial, Gap insurance for financed cars 2025

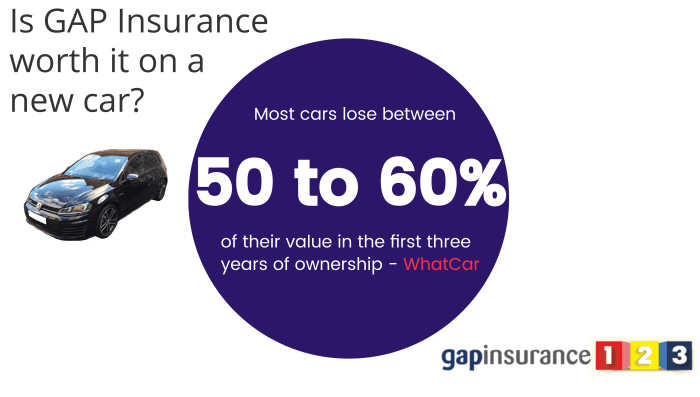

Gap insurance offers the most significant benefits when the value of your car depreciates quickly, which is common in the first few years after purchase. For example, if you finance a new car for 60 months and it’s totaled in the second year, the car’s value will likely have dropped considerably. In this case, gap insurance can prevent you from facing a substantial financial burden.

Similarly, if you finance a car with a longer loan term (72 months or more), the risk of owing more than the car’s worth increases, making gap insurance an even more attractive option. Another scenario where gap insurance shines is when purchasing a luxury car, which often depreciates faster than other vehicles.

Comparison of Gap Insurance Providers

Choosing a gap insurance provider requires careful consideration. While features and pricing can vary, several key factors remain consistent. Below is a sample comparison table (note: this is a sample and actual provider offerings may vary; always check with individual providers for current rates and details).

| Provider | Cost (Annual) | Coverage Limits | Deductible |

|---|---|---|---|

| Provider A | $250 – $400 | Up to $10,000 | $0 |

| Provider B | $300 – $500 | Up to $15,000 | $100 |

| Provider C | $200 – $350 | Up to $8,000 | $0 |

| Your Lender | Varies with Loan | Varies with Loan | Varies with Loan |

Gap Insurance Costs and Coverage in 2025: Gap Insurance For Financed Cars 2025

Gap insurance, while seemingly straightforward, presents a range of cost factors and coverage nuances. Understanding these aspects is crucial for making an informed decision about purchasing this supplemental auto insurance. The cost and extent of coverage can significantly vary based on several key elements.

Factors Influencing Gap Insurance Cost

Several factors determine the price of gap insurance. Your vehicle’s make, model, and year significantly impact the cost; newer vehicles, particularly those with higher initial values, typically command higher premiums due to a larger potential gap between the loan amount and the vehicle’s depreciated value. Your credit score also plays a role, with higher scores often translating to lower premiums.

The length of your loan term influences cost; longer terms generally mean higher premiums because the risk of a total loss during the loan period increases. Finally, the insurance company itself plays a role; different providers offer varying rates based on their risk assessments and business models. For example, a company with a strong history of low claims might offer lower premiums than a newer or less established company.

Typical Coverage Limits and Exclusions

Gap insurance typically covers the difference between what your auto insurance pays out for a totaled vehicle and the remaining balance on your auto loan. However, there are limitations. Coverage limits often align with the outstanding loan amount at the time of the total loss. Policies usually exclude certain types of damage, such as damage caused by wear and tear, negligence, or intentional acts.

Additionally, most policies will not cover modifications or aftermarket additions to your vehicle. Some policies may also have a deductible, which the policyholder is responsible for paying before the gap coverage kicks in. For example, a policy might cover up to $20,000 in gap coverage, but have a $500 deductible. This means the insurer would pay $19,500 in the event of a total loss, with the remaining $500 paid by the policyholder.

Scenarios Where Gap Insurance Covers the Shortfall

Consider this: Imagine you finance a new car for $30,000. After a year, the vehicle is totaled in an accident. Your comprehensive auto insurance only covers $20,000 due to depreciation. You still owe $10,000 on the loan. Gap insurance would cover this $10,000 difference, preventing you from being stuck with significant debt.

So, you’re looking at gap insurance for financed cars in 2025? That’s smart, especially if you’re in Texas, where figuring out your overall car costs is key. To get a better handle on your budget, check out the average monthly car insurance cost Average car insurance cost per month in Texas 2025 , which will help you plan for both insurance and gap coverage.

Getting both figured out early helps avoid nasty surprises down the road.

Another scenario involves a stolen vehicle that is never recovered. In this case, gap insurance would also cover the difference between the insurance payout and the outstanding loan amount.

Sample Gap Insurance Policy Summary

| Term | Description |

|---|---|

| Policy Number | 1234567890 |

| Policyholder | John Doe |

| Vehicle Information | 2025 Honda Civic, VIN: ABCDEF1234567 |

| Loan Amount | $25,000 |

| Coverage Limit | $25,000 |

| Deductible | $0 |

| Policy Term | 36 months |

| Exclusions | Wear and tear, intentional damage, aftermarket modifications |

Potential Hidden Fees or Additional Costs

It’s important to be aware of potential additional costs. Some insurance providers might charge administrative fees for processing a gap insurance claim. Others may include fees for early termination of the policy, should you pay off your loan early. Always carefully review the policy documents to understand all associated costs. These fees can range from a flat fee to a percentage of the premium.

It’s advisable to inquire about all potential fees upfront before purchasing the policy.

Purchasing Gap Insurance for Financed Cars in 2025

Securing gap insurance is a crucial decision for anyone financing a car in 2025. Understanding your options and making an informed choice can save you significant financial hardship in the event of a total loss. This section will guide you through the process of purchasing gap insurance, comparing different avenues and helping you navigate the specifics.

Where to Purchase Gap Insurance

Consumers have two primary avenues for purchasing gap insurance: directly from their car dealership or through an independent insurance provider. Dealerships often offer gap insurance as an add-on during the car buying process, while independent insurers specialize in providing various insurance products, including gap coverage.

Dealership vs. Independent Insurer: A Comparison

Choosing between a dealership and an independent insurer involves weighing several factors. Dealerships offer convenience; the purchase is often streamlined into the overall car buying experience. However, dealership gap insurance may be more expensive than policies from independent providers. Independent insurers frequently offer more competitive pricing and a wider range of coverage options. They may also provide more flexible payment plans.

Conversely, dealing with an independent insurer requires more legwork and may involve comparing multiple quotes.

Obtaining a Gap Insurance Quote: A Step-by-Step Guide

- Gather your information: This includes your vehicle identification number (VIN), loan details (loan amount, lender, and term), and your personal information (name, address, and driver’s license number).

- Contact potential providers: Reach out to your car dealership and several independent insurance companies. Many insurers allow you to get quotes online.

- Compare quotes: Carefully review each quote, paying close attention to the coverage details, premiums, and any exclusions.

- Review policy details: Before committing, thoroughly read the policy documents to understand the terms and conditions.

- Choose and purchase: Once you’ve selected the best policy for your needs, complete the application process and make the payment.

Required Documents for Gap Insurance Application

Typically, you’ll need to provide the following documents when applying for gap insurance:

- Vehicle identification number (VIN)

- Proof of vehicle ownership

- Copy of your loan agreement

- Driver’s license or other government-issued identification

- Proof of insurance (for your auto insurance)

Questions to Ask Before Purchasing Gap Insurance

Before committing to a gap insurance policy, consider these important questions:

- What is the exact coverage amount?

- Are there any exclusions or limitations on the coverage?

- What is the length of the coverage period?

- What is the cost of the policy and are there any additional fees?

- What is the claims process like, and how long does it typically take to settle a claim?

Gap Insurance and the 2025 Automotive Market

The automotive landscape is constantly shifting, and with it, the demand for financial products like gap insurance. Factors such as evolving financing options, changing depreciation rates, and technological advancements are all impacting the gap insurance market in significant ways, shaping its future trajectory in 2025 and beyond. Understanding these dynamics is crucial for both consumers and insurers.The increasing prevalence of longer loan terms and balloon payments in auto financing significantly impacts the need for gap insurance.

Longer loan terms mean higher overall interest paid, increasing the potential for a car’s value to depreciate below the loan amount before the loan is fully paid off. Balloon payments, which require a substantial lump sum payment at the end of the loan term, further exacerbate this risk. This makes gap insurance a more attractive proposition for consumers facing a larger potential shortfall.

Evolving Vehicle Financing Options and Gap Insurance Demand

The rise of alternative financing methods, such as lease buyouts and subscription services, also presents unique challenges and opportunities for gap insurance. For example, lease buyouts often involve a residual value that might not fully account for depreciation, making gap insurance a viable option to cover the difference. Subscription services, on the other hand, typically don’t involve financing in the traditional sense, thus reducing the need for gap insurance in this particular segment.

The market must adapt to these new financing models to offer relevant and valuable gap insurance solutions.

Vehicle Depreciation Rates and Gap Insurance Need

Changes in vehicle depreciation rates directly affect the likelihood of a borrower owing more on their loan than their vehicle is worth. Factors such as increased production of electric vehicles, advancements in automotive technology leading to faster obsolescence, and economic fluctuations can all impact depreciation rates. In a market with rapid depreciation, the demand for gap insurance is expected to increase as consumers seek protection against potential financial losses.

For example, the rapid technological advancements in the EV market could lead to higher depreciation rates for internal combustion engine vehicles, increasing the demand for gap insurance for those vehicles.

Emerging Trends in the Gap Insurance Market

Several trends are shaping the future of the gap insurance market. One key trend is the increasing use of data analytics and predictive modeling to better assess risk and personalize pricing. Insurers are leveraging large datasets to identify factors that influence the likelihood of a total loss and tailor premiums accordingly. Another trend is the development of more flexible and customizable gap insurance products, catering to the specific needs of different consumer segments.

For example, we might see gap insurance bundled with other financial products or tailored to specific vehicle types or financing structures.

Innovative Gap Insurance Products and Services

The insurance industry is witnessing the emergence of innovative gap insurance offerings. One example is the integration of gap insurance with telematics programs. This allows insurers to monitor driving behavior and offer discounts to safer drivers, reducing the overall cost of coverage. Another innovative approach is the development of “pay-as-you-go” gap insurance, where premiums are adjusted based on the actual risk profile of the insured vehicle, factoring in factors like mileage and location.

Technological Advancements and the Gap Insurance Landscape

Technology is transforming the gap insurance landscape. The increased use of digital platforms and online applications is streamlining the purchasing process, making it more convenient for consumers. Furthermore, blockchain technology could potentially improve transparency and security in the claims process, reducing fraud and ensuring faster payouts. Artificial intelligence is also playing a growing role, enabling insurers to automate tasks, personalize offerings, and improve risk assessment accuracy.

For example, AI-powered chatbots could handle routine inquiries, freeing up human agents to focus on more complex issues.

Illustrative Scenarios and Examples

Understanding gap insurance is best done through real-world examples. These scenarios illustrate the benefits, limitations, and claim process, helping you grasp its value in protecting your financial investment.

A Scenario Where Gap Insurance Prevented Significant Financial Loss

Imagine Sarah, a recent college grad, financed a brand-new 2023 SUV. Six months later, she was involved in a total loss accident. Her loan balance was $25,000, but the insurance payout for her totaled vehicle was only $20,000 due to depreciation. Without gap insurance, Sarah would have been responsible for the remaining $5,000. However, because she had gap insurance, the policy covered this $5,000 difference, preventing her from incurring a significant financial burden.

This allowed her to move on from the accident without the added stress of a substantial debt.

Gap Insurance Claim Calculation Example

Let’s say John financed a car for $30,000. After two years of payments, his loan balance is $22,000. Unfortunately, he’s involved in an accident that totals his car. His insurance company appraises the vehicle’s actual cash value (ACV) at $18,000. The gap between the loan balance ($22,000) and the ACV ($18,000) is $4,000.

John’s gap insurance policy covers this $4,000 difference, meaning his insurance company will pay out an additional $4,000 to his lender, settling his loan.

A Situation Where Gap Insurance Would NOT Cover the Loss

Gap insurance only covers the difference between the loan balance and the vehicle’s actual cash value after a total loss accident. It does not cover other losses, such as damage to the car from a minor accident, theft of personal belongings from the car, or medical expenses related to an accident. For example, if John had only sustained minor damage to his car, his gap insurance would not have covered the repair costs.

Similarly, if his car was stolen but recovered, gap insurance wouldn’t apply unless it was a total loss.

Visual Representation of Financial Impact

Imagine a simple bar graph. The left bar represents a total loss accident without gap insurance. It shows the loan balance (e.g., $25,000) as a tall bar, and a shorter bar representing the insurance payout (e.g., $20,000). The difference between the tops of these bars visually represents the $5,000 Sarah would owe. The right bar represents the same scenario but with gap insurance.

The insurance payout bar extends to meet the loan balance bar, showing the gap insurance covered the difference and eliminated the out-of-pocket expense.

Gap Insurance Claim Filing Process

Filing a gap insurance claim typically involves contacting your insurance company immediately after the accident. You’ll need to provide documentation including the police report, the insurance appraisal of your vehicle’s ACV, proof of your loan balance, and your gap insurance policy details. The timeline for claim processing varies by insurance company but usually takes several weeks. You should expect communication from your insurer throughout the process, updating you on the progress of your claim.

The insurer will work directly with your lender to settle the outstanding loan balance after the claim is approved.

Final Wrap-Up

So, is gap insurance right for you? That depends on your financial situation and how much risk you’re willing to take. Weighing the cost against the potential for a major financial headache is key. After reading this, you should be armed with the knowledge to make an informed decision. Don’t get blindsided by a total loss; understand your options and protect your wallet.