Best Credit Unions for Auto Loans in 2025? Yeah, that’s a HUGE question, especially with all the changes swirling around the auto loan market. Forget those stuffy bank loan officers – credit unions are where it’s at for scoring a sweet deal on your next ride. We’re diving deep into what makes credit unions awesome for auto loans in 2025, looking at interest rates, loan terms, and all the juicy details you need to snag the best financing.

Get ready to ditch the dealer’s financing and unlock serious savings.

This guide breaks down everything you need to know about getting an auto loan from a credit union in 2025. We’ll cover the key factors to consider – like interest rates, fees, and loan terms – and compare different credit unions to help you find the perfect fit. We’ll also explore the impact of your credit score and discuss different loan types.

Plus, we’ll look at future trends and how technology is changing the game. Let’s get this bread!

Introduction to Auto Loans from Credit Unions in 2025: Best Credit Unions For Auto Loans In 2025

The auto loan market in 2024 is a dynamic landscape shaped by fluctuating interest rates, evolving consumer preferences, and the increasing popularity of alternative financing options. Traditional banks remain major players, but competition from online lenders and, increasingly, credit unions is intensifying. Borrowers are faced with a wide array of choices, each with its own terms and conditions, making careful comparison shopping crucial.Choosing a credit union for an auto loan offers several key advantages over a traditional bank.

Credit unions are not-for-profit financial cooperatives owned by their members, meaning profits are often returned to members in the form of lower interest rates and fees. They often have a more personalized approach to lending, offering greater flexibility and potentially more favorable terms for borrowers with strong credit histories or those seeking smaller loan amounts. This member-centric focus can lead to a smoother, more supportive borrowing experience.

So, you’re hunting for the best credit unions for auto loans in 2025? That’s awesome! Before you sign on the dotted line, though, remember to check your insurance coverage; you’ll need it to drive that sweet new ride. Knowing the specifics of Georgia car insurance grace period laws is key, so you don’t get hit with penalties.

Getting your financing and insurance squared away early will make the whole car-buying process way smoother, ultimately helping you secure those killer credit union rates.

Potential Changes in the Auto Loan Market by 2025

The auto loan market is expected to undergo several significant shifts by 2025. Interest rate fluctuations will continue to play a major role, impacting both borrowing costs and the affordability of vehicles. The increasing adoption of electric vehicles (EVs) will likely reshape the market, with specialized financing options and potentially different lending criteria emerging for EV purchases. Technological advancements, such as the increased use of online loan applications and digital lending platforms, will further streamline the borrowing process.

For example, we might see more credit unions offering fully digital auto loan applications, eliminating the need for in-person visits. Furthermore, the rise of fintech companies and their partnerships with credit unions could introduce innovative financing models and improved customer experiences. The increasing integration of data analytics will likely lead to more personalized loan offers and risk assessments, resulting in potentially more tailored interest rates for individual borrowers.

For instance, a credit union might use data to identify borrowers with a history of responsible vehicle maintenance, offering them a slightly lower interest rate as a reward for their demonstrated financial responsibility.

Factors to Consider When Choosing a Credit Union

Choosing the right credit union for your auto loan in 2025 requires careful consideration of several key factors. It’s not just about the advertised interest rate; a deeper dive into the specifics of the loan and the credit union itself will save you money and headaches in the long run. Think of it like choosing a college – you need to look beyond the shiny brochures and really assess what fits your needs.Selecting a credit union involves comparing different aspects of their services to find the best fit for your financial situation and the specifics of your auto loan needs.

Failing to thoroughly investigate these factors could result in higher costs or less favorable loan terms.

Interest Rates and Fees

Interest rates are the most obvious factor, representing the cost of borrowing money. Credit unions often offer competitive rates compared to banks, but these rates vary based on your credit score, the loan term, and the type of vehicle. It’s crucial to compare the Annual Percentage Rate (APR), which includes interest and other fees, not just the interest rate itself.

Fees, such as application fees, origination fees, and prepayment penalties, can significantly impact the overall cost of the loan. Shop around and compare the total cost of the loan, including all fees, before making a decision. For example, a credit union advertising a lower interest rate might have higher origination fees, ultimately making another credit union with a slightly higher rate more cost-effective.

Loan Terms and Types

Credit unions typically offer various loan terms, ranging from 24 to 84 months or even longer. Shorter terms mean higher monthly payments but less interest paid overall. Longer terms mean lower monthly payments, but you’ll pay significantly more interest over the life of the loan. Understanding the implications of different loan terms is essential for budgeting and long-term financial planning.

They may also offer different loan types, such as new car loans, used car loans, and refinancing options. New car loans might have lower interest rates than used car loans due to lower risk for the lender. Refinancing allows you to potentially lower your interest rate if your credit score has improved since your initial loan. For instance, someone with a good credit score might qualify for a 48-month loan with a 4% APR for a new car, while someone with a lower score might only qualify for a 72-month loan with a 7% APR for a used car.

Credit Score’s Impact

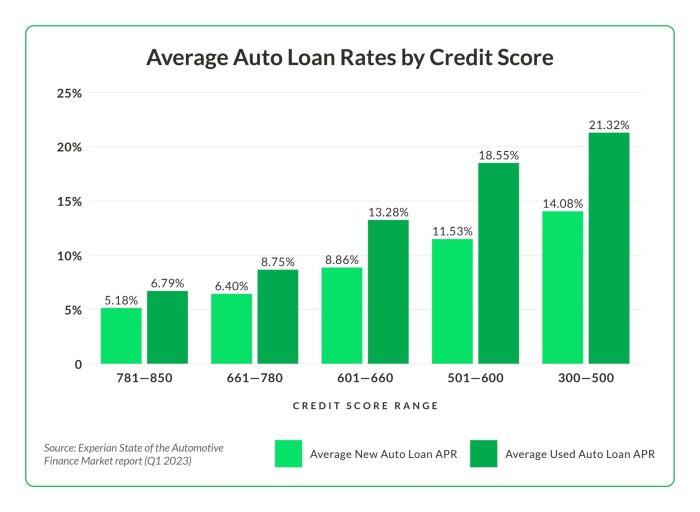

Your credit score plays a pivotal role in determining your eligibility for a loan and the interest rate you’ll receive. A higher credit score typically translates to lower interest rates and more favorable loan terms. Credit unions, like other lenders, use credit scores to assess your creditworthiness and risk. A lower credit score might result in loan denial or higher interest rates, significantly increasing the overall cost of borrowing.

Improving your credit score before applying for an auto loan can lead to substantial savings. For example, a difference of even 50 points in your credit score could mean a difference of 1-2 percentage points in your APR, leading to hundreds or even thousands of dollars in savings over the loan term. Checking your credit report beforehand and addressing any errors or negative marks is crucial.

Top Credit Unions for Auto Loans (2025 Projections)

Predicting the absolute best credit unions for auto loans in 2025 is tricky, as interest rates and specific offers fluctuate. However, based on current trends and historical performance, we can highlight several credit unions consistently providing competitive rates and excellent member services. This analysis focuses on those likely to remain top contenders.

Projected Top Credit Unions and Their Auto Loan Offers

The following table provides projected estimates for leading credit unions in 2025. Remember, these are projections based on current market trends and are subject to change. Always check directly with the credit union for the most up-to-date information.

| Credit Union | Estimated APR (72-month loan) | Loan Terms (Months) | Member Benefits |

|---|---|---|---|

| Navy Federal Credit Union | 5.5% – 7.5% | 12-84 | Low rates, various loan types, extensive online tools, excellent customer service. |

| PenFed Credit Union | 6.0% – 8.0% | 24-72 | Competitive rates, strong online presence, rewards programs for members, potential for discounts. |

| Alliant Credit Union | 5.8% – 7.8% | 24-72 | Nationwide access, competitive rates, strong online banking, various financial products. |

| USAA | 5.0% – 7.0% | 24-84 | Exclusive to military members and their families, consistently low rates, exceptional member service. |

Credit Union Auto Loan Application Processes

Each credit union offers a slightly different application process, but generally, they involve these steps: pre-qualification (checking your eligibility without impacting your credit score), formal application (providing financial details and vehicle information), credit check, loan approval or denial, and finally, loan funding. Many credit unions now offer completely online applications for convenience. For example, Navy Federal Credit Union is known for its user-friendly online platform, allowing for quick and easy applications and loan tracking.

PenFed offers both online and in-person options, catering to diverse member preferences. Alliant Credit Union provides a streamlined online process, emphasizing simplicity and speed. USAA, given its focus on military members, often offers personalized support through phone or in-person consultations alongside online options.

Examples of Successful Auto Loan Stories

While specific member stories are confidential, we can illustrate successful scenarios. Imagine a Navy Federal Credit Union member securing a 6.0% APR loan on a new car, utilizing their online tools to easily manage payments and track their progress. Another example could be a PenFed member leveraging their rewards program to reduce their interest rate slightly, ultimately saving money on their auto loan.

A prospective Alliant Credit Union member might find their nationwide branch network convenient for in-person assistance during the application process. Finally, a USAA member, a veteran, might appreciate the personalized service and competitive rates tailored to their needs. These are representative examples; individual experiences vary based on creditworthiness and loan specifics.

Analyzing Credit Union Loan Features

So you’re thinking about getting an auto loan from a credit union – smart move! But before you sign on the dotted line, understanding the nitty-gritty details of the loan itself is crucial. This section breaks down the key features you should be comparing to find the best deal for your situation.

Fixed-Rate vs. Variable-Rate Auto Loans

Credit unions, like banks, offer both fixed-rate and variable-rate auto loans. A fixed-rate loan means your interest rate stays the same for the entire loan term, providing predictable monthly payments. This stability is a major advantage, allowing you to budget effectively and avoid surprises due to fluctuating interest rates. Variable-rate loans, on the other hand, have an interest rate that adjusts periodically based on market conditions.

While this might mean a lower initial rate, you risk higher payments if interest rates rise during your loan term. The predictability of a fixed rate often outweighs the potential for a slightly lower initial rate with a variable option, especially in the current economic climate. For example, a fixed-rate loan might start at 6% and remain at 6% for the life of the loan, while a variable-rate loan might begin at 5.5% but increase to 7% or more if the prime rate increases.

Typical Fees Associated with Credit Union Auto Loans

Several fees can be associated with auto loans from credit unions. Understanding these upfront can help you compare offers more effectively and avoid unexpected costs. Origination fees are one common example; these are one-time charges that cover the administrative costs of processing your loan application. They can vary significantly between credit unions, so comparing this fee is essential.

Prepayment penalties are another potential cost. These penalties are charged if you pay off your loan early. While some credit unions don’t have prepayment penalties, others might charge a percentage of the remaining loan balance. Late payment fees are also standard, usually a flat fee charged for each missed payment. Finally, some credit unions may charge fees for things like additional services or specific loan features.

It’s always best to clarify all fees before committing to a loan.

Comparison of Credit Union Loan Features

Choosing the right auto loan requires careful consideration of various features. The following chart highlights the pros and cons of common features to aid in your decision-making process.

Locking down the best credit unions for auto loans in 2025 is key, especially if you’re planning a sweet ride upgrade. But remember, a killer loan rate is only half the battle; you’ll also need solid car insurance. Check out this list of Top-rated car insurance companies for seniors 2025 to find the best coverage for your new wheels.

Once you’ve got insurance sorted, you can totally focus on those awesome credit union loan rates.

| Loan Feature | Pros | Cons |

|---|---|---|

| Fixed Interest Rate | Predictable monthly payments; protects against rising interest rates; budgeting is easier. | May not have the lowest initial interest rate compared to variable rate loans. |

| Variable Interest Rate | Potentially lower initial interest rate; can benefit if interest rates fall. | Monthly payments can fluctuate; risk of significantly higher payments if interest rates rise; less predictable budgeting. |

| Longer Loan Term | Lower monthly payments; more affordable short-term. | Higher total interest paid over the life of the loan. |

| Shorter Loan Term | Lower total interest paid over the life of the loan; quicker payoff. | Higher monthly payments; may be less affordable short-term. |

| No Prepayment Penalty | Flexibility to pay off the loan early without penalty; saves on interest. | No disadvantage. |

| Prepayment Penalty | None. | Limits flexibility; may cost extra money if you pay off the loan early. |

Exploring Credit Union Membership Requirements

Gaining access to the often-better loan rates and terms offered by credit unions hinges on meeting their specific membership requirements. These requirements vary significantly depending on the credit union’s charter and the communities they serve. Understanding these nuances is crucial for finding the right credit union for your auto loan needs.

Credit unions typically operate under either a community or a group charter. Community charters usually serve a geographically defined area, while group charters cater to members sharing a common bond, such as employment at a specific company, membership in a particular organization, or residence within a specific neighborhood. The requirements for each type of charter are naturally quite different.

For example, a credit union chartered to serve employees of a specific university will only accept members who currently work for, or are retired from, that university. In contrast, a community charter might encompass all residents of a particular county.

Credit Union Membership Types and Eligibility Criteria

The specific eligibility criteria for each credit union are publicly available, typically on their website or through direct inquiry. However, some common membership requirements include:

- Geographic Location: Many credit unions require applicants to live or work within a specific geographic area, such as a city, county, or state.

- Employer Affiliation: Some credit unions restrict membership to employees, retirees, or family members of employees of a particular company or organization.

- Professional Affiliation: Certain credit unions are designed for members of specific professions or industries.

- Community Involvement: A few credit unions might require membership in a particular community organization or involvement in local activities.

- Family Membership: Once a person becomes a member, their immediate family members might also qualify for membership.

Finding a Credit Union That Meets Your Needs

Locating a credit union that matches your membership criteria requires a strategic approach. Simply searching online for “credit unions near me” might not be sufficient if you have specific membership requirements. A more targeted approach is needed.

For example, if you work for a specific company, start by searching for credit unions that serve employees of that company. If you are a member of a specific professional organization, investigate whether any credit unions cater to that profession. If geographic location is your primary concern, use online search engines with more specific location parameters, like zip code or neighborhood, in conjunction with s such as “credit union membership.”

Resources for Finding Suitable Credit Unions, Best credit unions for auto loans in 2025

Several online resources can assist in your search. These tools can help you filter your search by location, membership type, and other relevant factors. Remember to always verify the information found online with the credit union itself.

- The National Credit Union Administration (NCUA): The NCUA website provides a search tool to find credit unions based on location and other criteria. This is a reliable source of information about federally insured credit unions.

- Credit Union Websites: Many credit unions clearly Artikel their membership requirements on their websites. Check the “About Us” or “Membership” sections for details.

- Online Search Engines: Use targeted s and location-based search terms (e.g., “credit union near me for [profession]” or “credit union [city] membership requirements”) to refine your search.

- Referral Networks: Friends, family, and colleagues who are credit union members can provide valuable recommendations and insights into local credit unions and their respective membership eligibility.

Financial Literacy and Responsible Borrowing

Securing an auto loan is a significant financial commitment. Understanding responsible borrowing practices is crucial to avoid potential pitfalls and ensure a positive financial outcome. This section will Artikel key strategies for managing debt effectively and navigating the auto loan process with financial prudence.Responsible borrowing begins with a realistic assessment of your financial situation. Before applying for an auto loan, carefully analyze your income, expenses, and existing debts.

Determine how much you can comfortably afford to repay monthly without jeopardizing your financial stability. Consider factors like insurance, maintenance, and fuel costs beyond the loan payment itself. A budget meticulously tracking your income and expenditure is a crucial first step.

Auto Loan Amortization Schedule Example

An amortization schedule details your loan repayment plan, showing the principal and interest portions of each payment over the loan’s term. Let’s illustrate with a hypothetical example: Imagine a $20,000 auto loan at a 5% annual interest rate, amortized over 60 months (5 years). The monthly payment would be approximately $377. The first few months would have a larger interest portion and a smaller principal repayment.

As the loan progresses, the principal portion increases, and the interest portion decreases. A visual representation would be a table with columns for “Month,” “Beginning Balance,” “Payment,” “Interest Paid,” “Principal Paid,” and “Ending Balance.” The “Beginning Balance” for month one would be $20,000. The “Payment” would be $377 each month. The “Interest Paid” would be calculated based on the beginning balance and the interest rate (in this case, 5%/12).

The “Principal Paid” would be the difference between the payment and the interest paid. The “Ending Balance” would be the beginning balance minus the principal paid. This pattern continues for all 60 months, with the ending balance gradually decreasing until it reaches zero at the end of the loan term. This table clearly shows how your payments are allocated between interest and principal reduction over time.

Tools are available online that allow you to create personalized amortization schedules based on your specific loan terms.

Debt Management Strategies

Effective debt management involves proactive planning and disciplined execution. Prioritize high-interest debt, such as credit card debt, to minimize long-term interest costs. Explore options like debt consolidation to simplify payments and potentially lower interest rates. Automating loan payments ensures timely payments and avoids late fees, which can significantly impact your credit score. Regularly review your budget and track your progress.

Seek professional financial advice if needed to create a comprehensive debt management plan tailored to your circumstances. Remember that responsible borrowing is about maintaining a healthy financial balance and avoiding overwhelming debt.

Future Trends in Auto Loan Financing

The auto loan landscape is constantly evolving, driven by technological advancements and shifting consumer preferences. In 2025 and beyond, we can expect several significant trends to shape how people finance their vehicles, particularly through credit unions. These trends will impact everything from the application process to the overall cost and accessibility of loans.The integration of technology is fundamentally reshaping the auto loan experience.

This goes beyond simply having an online application; it’s about streamlining the entire process, improving efficiency, and enhancing the customer experience. This increased efficiency and transparency benefit both borrowers and lenders.

Technological Advancements in Auto Loan Processing

Technological advancements are dramatically altering the auto loan application and approval process. AI-powered systems are increasingly used to assess creditworthiness, automating much of the manual work previously involved. This leads to faster approval times and a more personalized lending experience. For example, some credit unions are already using algorithms to analyze a wider range of data points beyond traditional credit scores, potentially offering loans to individuals who might have been overlooked in the past.

Furthermore, the use of digital signatures and electronic document management systems simplifies paperwork and accelerates the overall process, creating a more seamless experience for borrowers. This automation also reduces the risk of human error, leading to more accurate and efficient loan processing.

The Role of Online Platforms and Digital Tools

Online platforms and digital tools are becoming the primary means by which borrowers interact with credit unions for auto loans. Credit union websites and mobile apps are increasingly sophisticated, offering features like loan calculators, pre-qualification tools, and secure online application portals. This shift towards digital channels empowers borrowers to shop around for the best rates and terms conveniently and at their own pace.

Furthermore, the use of online platforms facilitates a more transparent and efficient communication process between the borrower and the credit union, reducing delays and improving overall satisfaction. For instance, a borrower can track their application status in real-time, receive instant updates, and communicate with a loan officer through secure messaging systems within the platform. This enhanced accessibility and transparency are expected to become even more prevalent in the coming years.

Wrap-Up

So, there you have it – your roadmap to navigating the world of credit union auto loans in 2025. Remember, doing your homework is key. Compare rates, fees, and terms from several credit unions, and don’t be afraid to ask questions. With a little research and a solid plan, you can score an amazing auto loan that fits your budget and helps you cruise into the future with confidence.

Happy car shopping!