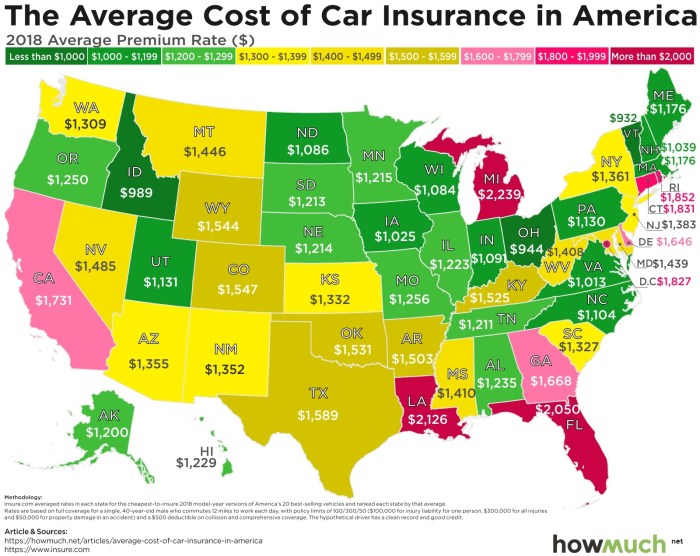

Average car insurance cost per month in Texas 2025? Yeah, that’s a big question for anyone hitting the road in the Lone Star State. Figuring out car insurance can feel like navigating a maze, especially with all the different factors at play – your driving record, the type of car you drive, even where you live. This deep dive breaks down everything you need to know about those costs, helping you make sense of it all and maybe even save some serious dough.

We’ll cover the average monthly premiums for different coverage levels, compare prices from major Texas insurers, and even look at how things like inflation and new laws might change costs in the future. We’ll also give you some pro tips for keeping your premiums down, so you can keep more money in your wallet and less in your insurance company’s.

Factors Influencing Car Insurance Costs in Texas

Predicting the exact cost of car insurance in Texas for 2025 is tricky, as rates fluctuate based on numerous factors. However, understanding these key influences can help you better anticipate your potential premiums. This overview examines the major components affecting your car insurance bill.

Driving History

Your driving record significantly impacts your insurance premiums. A clean record with no accidents or traffic violations will result in lower rates. Conversely, accidents and tickets, especially serious ones like DUIs, will drastically increase your premiums. Insurance companies view this as a higher risk, and they adjust your rates accordingly. For example, a single at-fault accident might lead to a 20-30% increase in your premiums for several years, while multiple incidents could result in even higher increases or even policy cancellation.

Figuring out the average car insurance cost per month in Texas for 2025 is tricky, with rates varying wildly. For seniors, though, finding the best deal is even more important, so checking out resources like Top-rated car insurance companies for seniors 2025 can be a huge help. Ultimately, understanding those senior-specific rates will help you better predict your own average monthly cost in Texas next year.

The severity of the accident also plays a role; a minor fender bender will have less impact than a serious collision. Similarly, speeding tickets, reckless driving citations, and other moving violations all contribute to higher premiums.

Vehicle Type

The type of car you drive directly affects your insurance costs. Generally, sports cars, luxury vehicles, and high-performance cars are more expensive to insure than sedans or smaller vehicles. This is because these vehicles are often more expensive to repair and replace, and they are statistically involved in more accidents. For example, insuring a high-performance sports car might cost significantly more than insuring a mid-sized sedan.

SUVs and trucks tend to fall somewhere in between, with larger trucks often commanding higher premiums due to their size and increased potential for damage. The vehicle’s safety features also play a role; cars with advanced safety technology like automatic emergency braking may qualify for discounts.

Figuring out your average car insurance cost per month in Texas for 2025 is tricky, especially since unexpected repairs pop up. For example, you might need to factor in the cost of fixing something like a broken CV axle; check out this link for an idea of what that might run you: Cost to replace a CV axle.

Knowing these potential extra expenses will help you budget accurately for your total car costs in Texas next year.

Age and Gender

Insurance companies use statistical data on age and gender to assess risk. Younger drivers, particularly those under 25, typically pay higher premiums due to their statistically higher accident rates. As drivers age and gain experience, their rates generally decrease. Gender also plays a role, though the impact varies by state and insurance company. Historically, males have faced higher premiums than females, reflecting statistical differences in accident rates and claims.

However, this gap is narrowing in many areas as driving habits and demographics shift.

Location

Where you live in Texas significantly impacts your insurance rates. Urban areas with higher population density and traffic congestion tend to have higher rates due to increased accident frequency and the higher cost of repairs in densely populated areas. Rural areas generally have lower rates due to less traffic and fewer accidents. The specific neighborhood or zip code can also influence premiums, as insurers consider crime rates and the frequency of claims in the area.

Living in a high-crime area, for example, might increase your rates due to a higher risk of theft or vandalism.

Average Monthly Premiums by Coverage Type

Understanding the average cost of car insurance in Texas in 2025 requires looking at the different coverage types. Premiums vary significantly depending on the level of protection you choose. This section breaks down average monthly costs for common coverage levels, providing a clearer picture of what you might expect to pay.

The figures presented below are estimates and can vary based on several factors including your driving record, age, location, vehicle type, and the specific insurance company. It’s crucial to obtain personalized quotes from multiple insurers to determine your precise premium.

Average Monthly Premiums by Coverage Level, Average car insurance cost per month in Texas 2025

The following table provides estimated average monthly costs for different coverage levels in Texas during 2025. These are categorized as low, medium, and high to reflect the range of premiums you might encounter. Remember, these are averages and your actual cost will depend on your individual circumstances.

| Coverage Type | Average Monthly Cost (Low) | Average Monthly Cost (Medium) | Average Monthly Cost (High) |

|---|---|---|---|

| Liability Only (Minimum Coverage) | $50 | $75 | $100 |

| Liability + Collision | $100 | $150 | $200 |

| Liability + Collision + Comprehensive | $125 | $180 | $250 |

Additional Coverage Options and Costs

Beyond the basic coverage types, many additional options can enhance your protection. These add to your premium, but can provide significant peace of mind in the event of an accident or unforeseen circumstances. The cost of these additions will vary by insurer and policy.

| Additional Coverage | Estimated Average Monthly Increase |

|---|---|

| Roadside Assistance | $5 – $15 |

| Rental Car Reimbursement | $10 – $20 |

| Uninsured/Underinsured Motorist Coverage | $15 – $30 |

| Medical Payments Coverage | $5 – $15 |

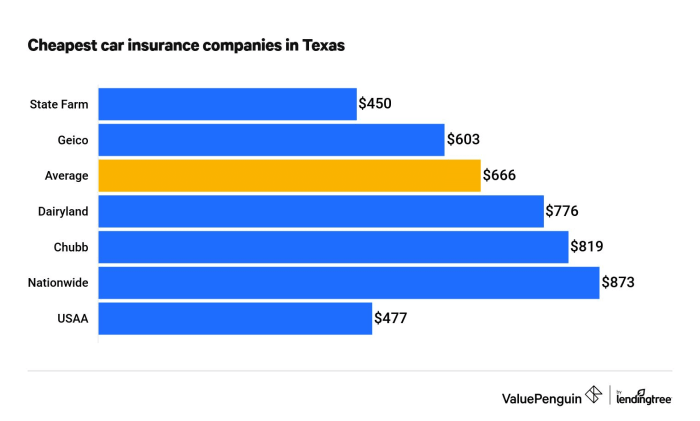

Comparison of Major Insurance Providers in Texas

Choosing the right car insurance provider in Texas can significantly impact your monthly budget. This section compares three major providers, highlighting their average premiums, coverage options, customer service, and rating systems to help you make an informed decision. Remember that actual premiums vary based on individual factors like driving history, vehicle type, and location.

This comparison focuses on State Farm, Geico, and Progressive, three of the largest and most well-known insurers in Texas. It’s crucial to remember that these are averages and your individual experience may differ.

Average Monthly Premiums by Provider

The following bullet points represent average monthly premiums for a standard liability policy in Texas, as estimated from various independent insurance comparison websites in late 2024. These are approximations and should not be considered definitive quotes.

- State Farm: $120 – $150. State Farm often emphasizes personalized service and a strong agent network.

- Geico: $100 – $130. Geico is known for its competitive pricing and streamlined online processes.

- Progressive: $110 – $140. Progressive offers a wide range of coverage options and is known for its innovative features like its Name Your Price® Tool.

Coverage Options and Customer Service

While all three providers offer standard liability, collision, and comprehensive coverage, there are nuances in their offerings and customer service approaches.

- State Farm: Generally known for its extensive agent network providing personalized service and potentially quicker claim processing through in-person interactions. They may offer more specialized coverage options, but potentially at a higher cost.

- Geico: Primarily operates online and through phone, emphasizing efficiency and affordability. Their online tools and quick claim processing are generally well-regarded, but in-person support may be limited.

- Progressive: Offers a blend of online and offline options, including a robust online platform and a network of agents. They’re recognized for their Name Your Price® Tool which allows customers to set a budget and find policies that fit. However, the range of coverage options and pricing can be complex.

Rating Systems and Discounts

Each provider uses different rating systems and offers varying discounts, influencing the final cost. Understanding these factors is crucial.

- State Farm: Uses a comprehensive rating system considering factors like driving history, age, location, and vehicle type. They offer discounts for safe driving, bundling policies, and other factors. Their specific discount programs may vary by location and agent.

- Geico: Emphasizes a transparent rating system, but specific details are less publicly available than State Farm’s. They offer discounts for good driving records, bundling, and sometimes for military personnel or students.

- Progressive: Uses a sophisticated algorithm for pricing, incorporating a wider range of data points. They heavily promote their discounts, including those for good student drivers, safe driving, and usage-based insurance programs.

Predicting Future Trends in Texas Car Insurance Costs: Average Car Insurance Cost Per Month In Texas 2025

Crystal balls are unfortunately out of stock, but we can still make some educated guesses about Texas car insurance costs in 2025. Several factors will likely influence premiums, creating a complex picture that’s far from a simple prediction. Analyzing these factors gives us a better understanding of potential scenarios.Predicting future car insurance costs involves considering various interacting elements.

The interplay between economic conditions, legislative changes, and evolving risk profiles within the state significantly impacts the final premium a driver pays. While pinpointing an exact figure is impossible, exploring these factors offers a plausible range of outcomes.

Factors Influencing Future Premiums

Several interconnected factors will significantly impact Texas car insurance costs in 2025. These include inflation, economic growth, changes in state regulations, and the frequency and severity of accidents.

Inflation’s impact on repair costs, medical expenses, and the overall cost of doing business for insurance companies will almost certainly push premiums higher. A robust economy might offset this somewhat, as increased employment could lead to fewer uninsured drivers. Conversely, a recession could lead to more drivers seeking lower coverage, potentially increasing the risk for insurers and leading to higher premiums for those who maintain full coverage.

State regulations, such as changes to minimum coverage requirements or the implementation of new driver safety programs, could significantly alter the insurance landscape, impacting both cost and availability. Finally, an increase in accidents due to factors like increased traffic or distracted driving will inevitably lead to higher claims and premiums.

Impact of Inflation and Economic Conditions

Inflation is a major wildcard. Rising repair costs for vehicles (especially with the increasing prevalence of advanced driver-assistance systems and electric vehicles), coupled with increased healthcare expenses, directly translate into higher claims for insurers. If inflation remains high, we can expect a substantial increase in premiums. Conversely, a period of economic downturn could result in fewer drivers on the road, reducing accident frequency and potentially mitigating some inflationary pressure.

However, a recession could also lead to more drivers opting for minimum coverage, increasing the risk pool for insurers and ultimately affecting rates for everyone. Consider, for example, the 2008 recession: while initially fewer accidents occurred, insurers still saw increased losses due to a higher percentage of uninsured drivers.

Potential Changes in State Regulations

Texas lawmakers could introduce legislation impacting car insurance costs. For instance, a law mandating increased minimum liability coverage would likely drive up premiums across the board. Conversely, new legislation promoting driver safety programs (like improved driver’s education or stricter distracted driving enforcement) could lead to a decrease in accidents and, consequently, lower premiums over time. The implementation of a no-fault insurance system, while potentially beneficial in some ways, could also lead to significant changes in the cost structure of insurance in the state.

The exact impact of any regulatory changes is highly dependent on the specifics of the legislation.

Scenarios for Average Monthly Premiums in 2025

Predicting exact figures is challenging, but based on different economic forecasts, we can Artikel plausible scenarios.

Scenario 1: Moderate Inflation, Steady Economic Growth. In this scenario, we might see a modest increase in average monthly premiums, perhaps in the range of 5-10%. This assumes relatively stable accident rates and no major regulatory changes. This is comparable to the average annual increase seen in recent years, adjusted for projected inflation.

Scenario 2: High Inflation, Economic Recession. This scenario paints a less optimistic picture. High inflation coupled with an economic downturn could lead to a more significant premium increase, potentially in the range of 15-20% or even higher. This would reflect the increased claims costs and potentially a higher proportion of uninsured drivers. The 2008 recession provides a real-world example of how economic downturns can impact insurance costs, even if in a slightly different way.

Scenario 3: Low Inflation, Strong Economic Growth. Conversely, a scenario with low inflation and strong economic growth could potentially lead to a smaller increase, perhaps only 2-5%, or even a slight decrease in some coverage types. This scenario is less likely given current economic trends but serves as a useful counterpoint to illustrate the range of possibilities.

Tips for Reducing Car Insurance Costs in Texas

Saving money on car insurance in Texas is definitely achievable. By making smart choices and understanding how insurers assess risk, you can significantly lower your premiums. This section Artikels practical strategies to help you achieve lower monthly payments.

Several factors influence your car insurance rates. Understanding these factors empowers you to make informed decisions that directly impact your premium. By focusing on controllable aspects like driving history, credit score, and policy choices, you can actively manage your insurance costs.

Improving Driving History and Credit Score

Your driving record and credit score are major factors in determining your insurance rates. Insurers view a clean driving record and good credit as indicators of lower risk. Improving these areas can lead to substantial savings.

- Maintain a clean driving record: Avoid speeding tickets, accidents, and DUI convictions. Even a single incident can significantly increase your premiums. Defensive driving courses can sometimes lower your rates after an infraction.

- Improve your credit score: Pay bills on time, keep credit utilization low, and monitor your credit report regularly for errors. A higher credit score demonstrates financial responsibility, which insurers see as a positive factor.

- Consider a usage-based insurance program: Some insurers offer programs that track your driving habits. Safe driving behaviors, such as avoiding harsh braking and speeding, can lead to discounts.

Choosing a Higher Deductible

Your deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. Opting for a higher deductible means you’ll pay more in the event of an accident, but your monthly premiums will be lower. This is a trade-off – weighing the risk of a larger upfront payment against lower monthly costs.

For example, a $1000 deductible will generally result in lower monthly premiums than a $500 deductible. Carefully consider your financial situation and risk tolerance before choosing a deductible. A higher deductible might be a good option if you have an emergency fund to cover potential expenses.

Bundling Insurance Policies

Bundling your home and auto insurance policies with the same insurer is a common way to save money. Many companies offer discounts for bundling, rewarding customers for their loyalty and consolidating their business.

The discount amount varies depending on the insurer and the specific policies bundled. It’s always a good idea to compare quotes from different insurers, both bundled and unbundled, to determine the best value. For instance, State Farm or Allstate might offer a significant percentage discount for bundling home and auto insurance.

End of Discussion

So, what’s the bottom line on average car insurance costs in Texas in 2025? While predicting the future is always tricky, by understanding the key factors that influence premiums – from your driving history to the type of car you drive – you can make informed decisions and potentially save a ton. Remember to shop around, compare quotes, and don’t be afraid to negotiate! With a little savvy, you can find a policy that fits your budget and your needs.

Happy driving (and saving!).