Cheapest car insurance in Michigan no-fault 2025 – Cheapest car insurance in Michigan no-fault 2025? Yeah, that’s a HUGE question for anyone in the Mitten State. Michigan’s no-fault system is, let’s just say,

-unique*. It’s all about personal injury protection (PIP), which covers your medical bills and lost wages regardless of who caused the accident. But that also means premiums can be, well, pretty hefty.

This guide breaks down how to navigate the system and find the best rates in 2025, covering everything from understanding your coverage options to scoring those sweet, sweet discounts.

We’ll dive into the factors that impact your car insurance costs – your driving record, your car, even your age and gender play a role. We’ll also look at how Michigan’s no-fault laws might change in 2025 and what that means for you. Think of this as your survival guide to affordable car insurance in the Great Lakes State.

Get ready to become a car insurance ninja!

Understanding Michigan’s No-Fault System

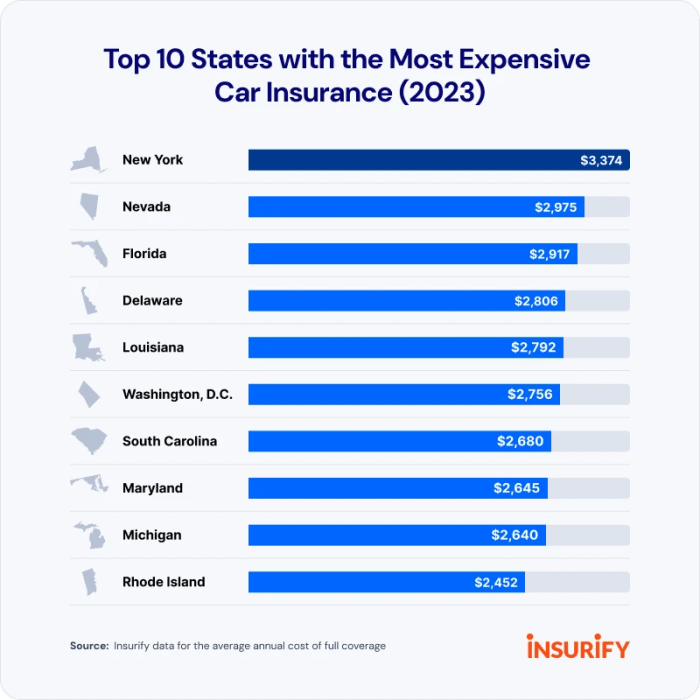

Michigan’s no-fault auto insurance system is a unique system in the United States, designed to ensure that accident victims receive prompt medical and wage-loss benefits regardless of fault. This means that your own insurance company, not the at-fault driver’s insurance company, covers your medical bills and lost wages after an accident, regardless of who caused the crash. However, it’s not a completely free-for-all; there are limits and specific rules you need to understand.This system, while aiming for fairness and efficiency, has also led to some high insurance costs, a point that’s been heavily debated in recent years.

Understanding its mechanics is key to navigating the process and finding the best and most affordable coverage for your needs.

Mandatory Coverages Under Michigan No-Fault Law

Michigan law mandates several types of insurance coverage. Failure to carry these minimum coverages can result in significant penalties. These coverages protect you and your passengers, regardless of fault in an accident. The mandatory coverages are designed to ensure basic financial protection for those injured in car accidents. They are not optional and must be maintained for your vehicle to be legally operated in the state.

- Personal Injury Protection (PIP): This covers medical expenses, lost wages, and replacement services (like childcare) for you and your passengers, regardless of who caused the accident. The amount of PIP coverage you choose directly impacts your premium.

- Property Protection Insurance (PPI): This covers damage to your vehicle and other property in an accident. It’s important to note that PPI only covers damage to

-your* vehicle and property, not the other party’s. - Uninsured/Underinsured Motorist Coverage: This protects you if you’re involved in an accident with an uninsured or underinsured driver. It helps cover your medical bills and other losses that the at-fault driver’s insurance might not fully cover.

Types of Personal Injury Protection (PIP) Coverage

PIP coverage in Michigan comes in different levels, offering varying degrees of protection and impacting the cost of your insurance premiums. Choosing the right level of PIP coverage is a crucial decision, balancing the level of protection with affordability. Higher coverage limits mean higher premiums, but also greater financial security in the event of a serious accident.

- Unlimited PIP: This offers the most comprehensive coverage, paying for all medical expenses and lost wages without a cap. However, it is also the most expensive option.

- Specific Dollar Limit PIP: This provides coverage up to a specified dollar amount (e.g., $50,000, $250,000). Once that limit is reached, coverage ends, leaving the injured party potentially responsible for further expenses.

Examples of Situations Where No-Fault Insurance Applies

Michigan’s no-fault system applies to a wide range of situations. Understanding these examples helps clarify the breadth of its coverage. The key is that your own insurance company will typically handle your claims, regardless of fault.

- A rear-end collision where you are at fault: Your PIP coverage will pay for your medical bills and lost wages, even though you caused the accident.

- A single-car accident: Your PIP coverage will still apply, even if no other vehicle was involved. This could be due to hitting a deer, for example.

- An accident where the other driver is uninsured: Your uninsured/underinsured motorist coverage will step in to cover your losses, supplementing your PIP benefits.

- An accident where the other driver flees the scene: Your PIP coverage will still apply; you will not be left without coverage simply because the other driver cannot be identified.

Factors Affecting Car Insurance Costs in Michigan

Getting the cheapest car insurance in Michigan can feel like navigating a maze, especially with the state’s unique no-fault system. Many factors influence your premium, and understanding them is key to finding the best deal. This section will break down the major players in determining your car insurance costs.

Driving History’s Impact on Premiums

Your driving record is a significant factor in determining your insurance rates. Insurance companies view it as a strong indicator of your risk as a driver. Accidents and traffic violations significantly increase your premiums. The more serious the incident, the greater the impact. For example, a DUI conviction will likely result in a much higher increase than a minor speeding ticket.

Multiple incidents within a short period will compound the effect, potentially leading to significantly higher premiums or even policy cancellation.

Age and Gender as Rate Determinants

Statistically, younger drivers and males tend to have higher accident rates than older drivers and females. Consequently, insurance companies often charge them more. This is a broad generalization, and individual driving records significantly influence the final premium. However, the age and gender demographics are statistically weighted into the initial risk assessment. For example, a 16-year-old male driver will generally pay considerably more than a 50-year-old female driver with a clean record, all other factors being equal.

Vehicle Type and Insurance Costs

The type of car you drive also affects your insurance premiums. Sports cars and luxury vehicles are often more expensive to insure because they are more likely to be involved in accidents, and repairs are typically more costly. Conversely, smaller, less expensive vehicles generally come with lower insurance rates. For example, insuring a high-performance sports car will likely cost significantly more than insuring a compact economy car, even if both drivers have identical driving records.

Factors Affecting Michigan Car Insurance Costs

| Factor | Impact on Cost | Example | Mitigation Strategy |

|---|---|---|---|

| Driving History | Higher premiums for accidents and tickets | A DUI conviction significantly raises premiums. | Maintain a clean driving record, take defensive driving courses. |

| Age and Gender | Younger drivers and males often pay more. | A 16-year-old male will generally pay more than a 40-year-old female. | Maintain a clean driving record, consider bundling insurance policies. |

| Vehicle Type | Expensive cars cost more to insure. | A luxury SUV will be more expensive to insure than a compact car. | Choose a vehicle with lower insurance ratings. |

| Location | Higher crime rates in certain areas lead to higher premiums. | Living in a high-crime city will generally result in higher premiums. | Consider the crime rate when choosing a residence. (This is less controllable than other factors) |

Finding Affordable Car Insurance Options

Finding the cheapest car insurance in Michigan can feel like navigating a maze, especially with the complexities of the no-fault system. But with a strategic approach and some diligent research, you can significantly reduce your premiums. This section Artikels effective strategies to help you find the best deal on your car insurance.

Successfully securing affordable car insurance involves a multi-pronged approach. It’s not just about comparing prices; it’s about understanding your needs, shopping around strategically, and carefully reviewing policy details. This ensures you get the best coverage at the most competitive price, without sacrificing essential protection.

Comparing Quotes from Different Insurers

A systematic approach to comparing quotes is crucial for finding the best deal. Start by gathering quotes from at least three to five different insurers. Don’t just focus on the price; compare coverage details, deductibles, and policy terms. This methodical comparison allows for a more informed decision. A simple spreadsheet can help you organize the information effectively.

For example, list the insurer’s name, the premium amount, the coverage details (liability limits, personal injury protection (PIP), uninsured/underinsured motorist coverage, collision, and comprehensive), and the deductible for each.

Utilizing Online Comparison Tools, Cheapest car insurance in Michigan no-fault 2025

Online comparison tools offer a convenient way to quickly gather quotes from multiple insurers. These tools typically require you to input basic information about yourself and your vehicle, after which they provide a list of potential quotes. However, remember that these tools often present only a snapshot of available options and may not include every insurer operating in Michigan.

It’s always advisable to contact insurers directly to confirm quotes and discuss policy details beyond what the comparison tool displays.

Understanding Policy Terms and Conditions

Before committing to a policy, thoroughly review the terms and conditions. Pay close attention to the specific coverage details, deductibles, exclusions, and any additional fees or surcharges. Understanding these aspects will help you make an informed decision and avoid unexpected costs or limitations down the line. Misunderstanding a policy can lead to costly consequences later on, so taking the time to fully understand it is critical.

For instance, a higher deductible will usually lower your premium, but you’ll pay more out-of-pocket in the event of a claim.

Essential Questions to Ask Insurance Providers

Before choosing a policy, asking specific questions to insurance providers is vital. This ensures you understand exactly what you’re paying for and what level of protection you’re receiving.

Asking these questions empowers you to make an informed decision. Don’t hesitate to seek clarification on anything you don’t understand.

Finding the cheapest car insurance in Michigan no-fault 2025 can be a total headache, especially if you’re new to the whole driving thing. Rates are usually higher for younger drivers, so if you’re under 25, check out this resource for some tips on finding the best insurance: Best insurance for first-time drivers under 25. Knowing that can help you navigate the Michigan no-fault system and find the best deal for your situation.

Ultimately, comparing quotes is key to securing the cheapest car insurance in Michigan no-fault 2025.

- What are the specific coverage limits for liability, PIP, and uninsured/underinsured motorist coverage?

- What is the deductible for collision and comprehensive coverage?

- Are there any discounts available based on my driving record, vehicle features, or other factors?

- What is the process for filing a claim, and what are the expected wait times?

- What are the payment options available, and are there any penalties for late payments?

- What is the insurer’s customer service rating and complaint resolution process?

Discounts and Savings Opportunities

Saving money on your Michigan no-fault car insurance is definitely a priority, and thankfully, there are several ways to lower your premiums. Many companies offer a range of discounts, and understanding these can significantly impact your overall cost. Let’s explore some common strategies and the potential savings involved.

Common Discounts Offered by Michigan Car Insurance Companies

Michigan car insurance providers offer a variety of discounts to incentivize safe driving and responsible insurance practices. These discounts can substantially reduce your premiums, making insurance more affordable. Common discounts include good driver discounts (for maintaining a clean driving record), multi-car discounts (for insuring multiple vehicles under one policy), and discounts for safety features in your car (such as anti-theft devices or advanced safety technology).

Other common discounts include discounts for bundling insurance policies (home and auto), and discounts for completing defensive driving courses. The specific discounts offered and their value can vary between insurance companies, so it’s crucial to shop around and compare.

Qualifying for Discounts Based on Driving Habits

Many insurance companies now utilize telematics programs to monitor your driving behavior. These programs typically involve installing a small device in your car or using a smartphone app that tracks your driving habits, such as speed, braking, and mileage. By demonstrating safe driving practices through these programs, you can often qualify for significant discounts. For example, a driver who consistently maintains a safe speed and avoids harsh braking might receive a discount of 10-20% or more.

The exact discount amount depends on your driving score and the specific insurance provider’s program. It’s important to review the terms and conditions of any telematics program before enrolling, as data collection practices vary.

Potential Savings from Bundling Insurance Policies

Bundling your home and auto insurance policies with the same company is another excellent way to save money. Insurance companies often offer significant discounts for bundling, as it simplifies their administrative processes and reduces risk. The savings from bundling can be substantial, sometimes reaching 15-25% or more off your total premium. For example, if your annual auto insurance premium is $1200 and your home insurance premium is $800, bundling could potentially save you $200-$300 annually.

This is a simple way to reduce your overall insurance costs without compromising coverage.

Comparative Table of Discounts and Potential Savings

| Discount Type | Eligibility Criteria | Estimated Savings |

|---|---|---|

| Good Driver Discount | Clean driving record (no accidents or tickets in a specified period) | 5-20% |

| Multi-Car Discount | Insuring two or more vehicles with the same company | 10-25% |

| Safety Feature Discount | Vehicle equipped with anti-theft devices or advanced safety features (e.g., airbags, anti-lock brakes) | 5-15% |

| Telematics Program Discount | Participation in a telematics program and demonstrating safe driving habits | 10-25% |

| Bundling Discount (Home & Auto) | Insuring both home and auto with the same company | 15-25% |

Navigating the 2025 Insurance Landscape

The Michigan no-fault insurance system underwent significant changes in recent years, and 2025 will likely see continued adjustments and their ripple effects on the market. Understanding these potential shifts is crucial for drivers to make informed decisions about their insurance coverage. While predicting the exact details is challenging, we can examine anticipated changes and their potential impact on costs and consumer strategies.Predicting the precise nature of Michigan’s no-fault law changes in 2025 is difficult due to the ongoing legislative and judicial processes.

However, based on current trends and past reforms, several key areas are likely to experience further adjustments.

Anticipated Changes to Michigan’s No-Fault Laws

Discussions surrounding further modifications to the 2019 reforms are ongoing. These may involve adjustments to the limits on medical care coverage, potentially leading to higher or lower premiums depending on the specific changes implemented. Further refinement of the fee schedule for medical providers is also a possibility, which could impact the cost of claims and consequently, insurance premiums.

Finally, there might be changes to the dispute resolution process for no-fault claims, aiming to streamline the system and reduce costs. For example, the state might introduce stricter guidelines for evaluating the legitimacy of claims, leading to potential reductions in fraudulent claims and subsequently, premiums.

Potential Impacts of Changes on Car Insurance Costs

The impact of these changes on car insurance costs is complex and depends heavily on the specific nature of the legislation. For instance, reducing the cap on medical coverage could lead to lower premiums for some drivers, especially those who choose lower coverage limits. Conversely, increased scrutiny on medical billing practices might initially lead to higher premiums as insurers adjust to the new regulations, but could eventually lead to lower costs as fraudulent claims are reduced.

Similarly, improvements to the dispute resolution system could lead to faster claim processing and lower administrative costs for insurers, potentially translating into lower premiums for consumers. However, if these changes lead to increased litigation, it could offset any cost savings.

Preparing for Potential Changes

Consumers can prepare for these potential changes by actively monitoring legislative updates and consulting with their insurance agents. Staying informed about proposed changes allows for proactive adjustments to coverage levels and the selection of insurance providers. Shopping around and comparing quotes from multiple insurers is always a good strategy to secure the best rates. Drivers should also review their current coverage to ensure it aligns with their needs and risk tolerance.

For example, a driver with a history of accidents or injuries might consider maintaining higher coverage limits, even if premiums increase slightly. Understanding your personal risk profile and its potential impact under new legislation is key to making informed decisions.

Finding the cheapest car insurance in Michigan with no-fault coverage in 2025 can be a real headache, but there are ways to lower your premiums. One major way to save is by taking advantage of discounts, and checking if you qualify for a good student discount by looking at the eligibility requirements on this site: Good student discount eligibility 2025.

Snagging that discount can seriously help you land that cheapest car insurance rate in Michigan for 2025.

Impact on Different Driver Profiles

The impact of these changes will vary depending on individual driver profiles. For example, a young, inexperienced driver with a history of accidents might see a larger increase in premiums due to increased scrutiny on claims and potential adjustments to the risk assessment models used by insurance companies. Conversely, an older driver with a clean driving record and minimal healthcare needs might experience a modest decrease in premiums if the changes lead to a reduction in overall healthcare costs within the system.

A driver who frequently utilizes their car for business purposes might also see different impacts compared to a driver who primarily uses their car for commuting. These varying impacts underscore the importance of individual assessment and proactive planning.

Illustrative Scenarios

Let’s look at some real-world examples to illustrate how different factors can impact your Michigan no-fault car insurance costs in 2025. These scenarios are based on average premiums and coverage limits, and your actual costs may vary. Remember to always get personalized quotes from multiple insurers.

Minimum vs. Higher Coverage Levels

Consider two drivers, both 30 years old with clean driving records, living in the same suburban area of Michigan. Driver A chooses the minimum required coverage under Michigan’s no-fault law, while Driver B opts for significantly higher coverage limits. Let’s assume Driver A’s minimum coverage policy costs approximately $1,500 annually, with $20,000 in personal injury protection (PIP) and $25,000 in property damage liability.

Driver B, on the other hand, selects a policy with $500,000 in PIP and $300,000 in property damage liability, costing around $3,000 annually. This example demonstrates the considerable difference in premium cost associated with increased coverage. The higher premium reflects the significantly greater financial protection offered by Driver B’s policy. In the event of a serious accident, Driver B would have far greater financial security.

Impact of a Minor Accident on Premiums

Imagine a young driver, 22 years old, with a clean driving record, who gets into a fender bender causing $1,000 in damage to another vehicle. Before the accident, their annual premium was $2,000. After the accident, even a minor one, their insurer may increase their premium by 15-20%, resulting in a new annual premium of approximately $2,300 to $2,400.

This increase reflects the added risk associated with the accident, even if it was relatively minor. The impact on premiums can vary depending on the specifics of the accident, the driver’s history, and the insurance company’s policies.

Savings from Bundling Insurance Policies

Let’s say the same 22-year-old driver also needs homeowners insurance. Purchasing both auto and homeowners insurance separately might cost $2,000 (auto) and $800 (homeowners) annually, totaling $2,800. However, by bundling both policies with the same insurer, they could receive a significant discount, perhaps 15-20%, reducing the total annual cost to around $2,240 to $2,320. This example highlights the substantial savings achievable through bundling, making it a financially smart decision for many drivers.

The exact savings will vary depending on the insurer and the specific policies.

Conclusion: Cheapest Car Insurance In Michigan No-fault 2025

So, finding the cheapest car insurance in Michigan in 2025 isn’t about magic; it’s about smart shopping and understanding the system. By comparing quotes, leveraging discounts, and knowing what to ask your insurer, you can significantly lower your premiums. Remember, being informed is your best defense against sky-high insurance costs. Don’t just settle for any policy; find one that fits your needs and your budget.

Happy driving (and saving!)